Note: Data refer to FDIC-insured commercial and savings banks that were

closed or received FDIC assistance.

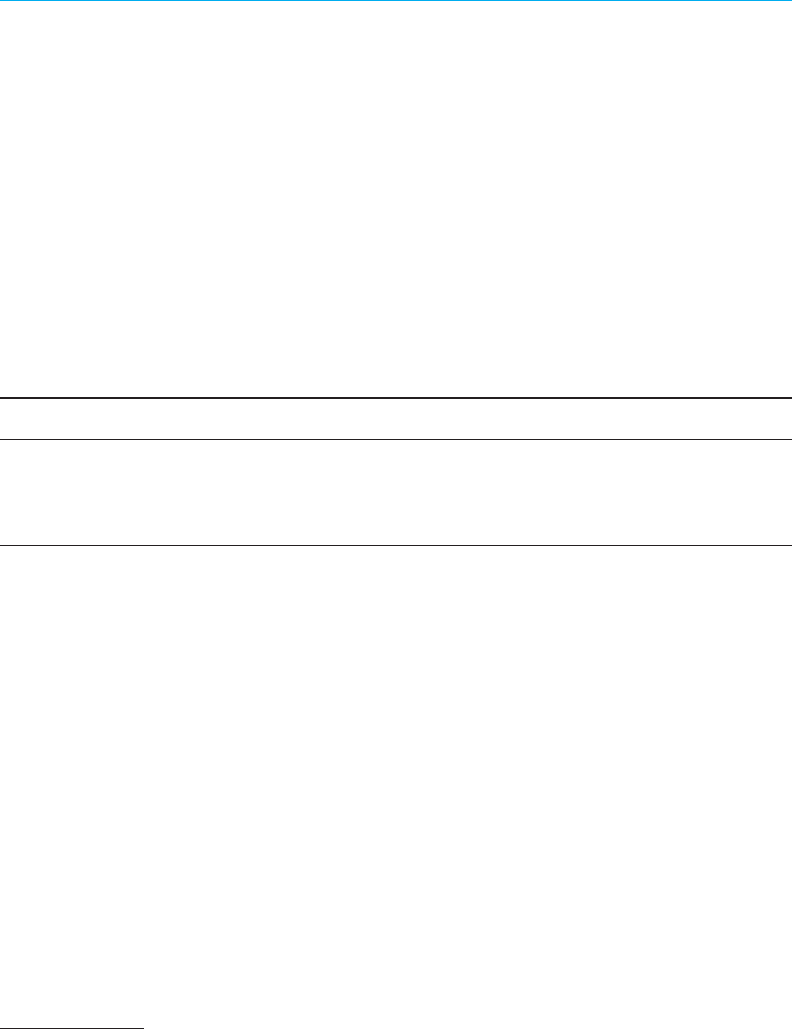

Figure 1.1

Number of Bank Failures, 1934–1995

Number

1935 1945 1955 1965 1975 1985 1995

0

50

100

150

200

250

300

Chapter 1

The Banking Crises of the

The Banking Crises of the

1980s and Early 1990s:

1980s and Early 1990s:

Summar

Summar

y and Implications

y and Implications

Introduction

The distinguishing feature of the history of banking in the 1980s was the extraordi-

nary upsurge in the number of bank failures. Between 1980 and 1994 more than 1,600

banks insured by the Federal Deposit Insurance Corporation (FDIC) were closed or re-

ceived FDIC financial assistancefar more than in any other period since the advent of

federal deposit insurance in the 1930s (see figure 1.1). The magnitude of bank failures dur-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

4 History of the EightiesLessons for the Future

ing the 1980s put severe, though temporary, strains on the FDIC insurance fund; raised ba-

sic questions about the effectiveness of the bank regulatory and deposit insurance systems;

and led to far-reaching legislative and regulatory actions.

1

This chapter summarizes the findings and implications of History of the Eighties

Lessons for the Future: An Examination of the Banking Crises of the 1980s and Early

1990s, a study conducted by the FDICs Division of Research and Statistics to analyze var-

ious aspects of the 198094 experience. The four sections of this summary deal with (1) the

factors underlying the rapid rise in the number of bank failures; (2) the regulatory issues

raised by this experience; (3) questions that remain open despite the legislative and regula-

tory remedies adopted between 1980 and 1994; and (4) concluding comments.

The Rise in the Number of Bank Failures in the 1980s:

The Economic, Legislative, and Regulatory Background

The rise in the number of bank failures in the 1980s had no single cause or short list

of causes. Rather, it resulted from a concurrence of various forces working together to pro-

duce a decade of banking crises. First, broad national forceseconomic, financial, legisla-

tive, and regulatoryestablished the preconditions for the increased number of bank

failures. Second, a series of severe regional and sectoral recessions hit banks in a number of

banking markets and led to a majority of the failures. Third, some of the banks in these mar-

kets assumed excessive risks and were insufficiently restrained by supervisory authorities,

with the result that they failed in disproportionate numbers.

Economic and Financial Market Environment

During most of the 1980s, the performance of the national economy, as measured by

broad economic aggregates, seemed favorable for banking. After the 198082 recession the

national economy continued to grow, the rate of inflation slowed, and unemployment and

interest rates declined. However, in the 1970s a number of factors, both national and inter-

national, had injected greater instability into the environment for banking, and these earlier

developments were directly or indirectly generating challenges to which not all banks

would be able to adapt successfully. In the 1970s, exchange rates among the worlds major

currencies became volatile after they were allowed to float; price levels underwent major

increases in response to oil embargoes and other external shocks; and interest rates varied

widely in response to inflation, inflationary expectations, and anti-inflationary Federal Re-

serve monetary policy actions.

1

Although this study is devoted to banking, it is appropriate to recall that the thrift industry suffered an even greater ca-

tastrophe. In 1980 there were 4,039 savings institutions; approximately 1,300 savings institutions failed during the 198094

period. This high proportion of failures led to the demise of the fund that insured savings institution deposits, and imposed

heavy costs on surviving institutions and on taxpayers.

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 5

Developments in the financial markets in the late 1970s and 1980s also tested the

banking industry. Intrastate banking restrictions were lifted, allowing new players to enter

once-sheltered markets; regional banking compacts were established; and direct credit mar-

kets expanded.

2

In an environment of high market rates, the development of money market

funds and the deregulation of deposit interest rates exerted upward pressures on interest ex-

pensesparticularly for smaller institutions that were heavily dependent on deposit fund-

ing. Competition increased from several directions: within the U.S. banking industry itself

and from thrift institutions, foreign banks, and the commercial paper and junk bond mar-

kets. The banking industrys share of the market for loans to large business borrowers de-

clined, partly because of technological innovations and innovations in financial products.

3

As a result, many banks shifted funds to commercial real estate lendingan area involving

greater risk. Some large banks also shifted funds to less-developed countries and leveraged

buyouts, and increased their off-balance-sheet activities.

Condition of Banking on the Eve of the 1980s

Yet on the eve of the 1980s most banks gave few obvious signs that the competitive

environment was becoming more demanding or that serious troubles lay ahead. At banks

with less than $100 million in assets (the vast majority of banks), net returns on assets

(ROA) rose during the late 1970s and averaged approximately 1.1 percent in 1980a level

that would not be reached again until 1993, after the wave of bank failures had receded (see

figure 1.2).

4

For this group of banks, net returns on equity (ROE) in 1980 were also high by

historical standards, equity/asset ratios were moving gradually upward, and charge-offs on

loans averaged approximately what they would again in the early 1990s. The fact that key

performance ratios in 1980 compared favorably with those in 199394a period of extra-

ordinary health and profitability in banking that has continued to the present (mid-1997)

emphasizes the absence of obvious problems at most banks at the beginning of the eighties.

Large banks, however, showed clearer signs of weakness. In 1980 ROA and equity/as-

sets ratios were much lower for banks with more than $1 billion in assets than for small

2

Many of these developments are discussed in Allen N. Berger, Anil K. Kashyap, and Joseph M. Scalise, The Transforma-

tion of the U.S. Banking Industry: What a Long, Strange Trip Its Been, Brookings Papers on Economic Activity 2 (1995).

3

Between 1980 and 1990, commercial paper outstanding increased from 7 percent of bank commercial and industrial loans

(C&I) to 19 percent.

4

Data in figure 1.2 are unweighted averages of individual bank ratios. Use of median values or averages weighted by assets

reveals broadly similar trends, except that medians are less affected by extreme values and tend to be less volatile than un-

weighted averages, while weighted averages are dominated by larger banks in each size group. The data in figure 1.2 are for

banks with assets greater than $1 billion (large banks) or less than $100 million (small banks) in each year; thus, the num-

ber of banks included in the two size groups varies from year to year. In 1980, there were 192 banks with assets greater than

$1 billion and 12,735 banks with assets less than $100 million. In 1994, the comparable figures were 392 banks and 7,259

banks. Asset data are not adjusted for inflation.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

6 History of the EightiesLessons for the Future

Loans and Leases/Assets

Net Loan Charge-Offs/Loans

Note: Data are unweighted averages of individual FDIC-insured commercial and savings bank ratios. Large banks are those

with assets greater than $1 billion in any given year. Small banks are those with assets less than $100 million in any given year.

Figure 1.2

Bank Performance Ratios, 1973 94–19

ROE

ROA

All Banks

Large Banks Small Banks

Equity/Assets

1974 1978 1982 1986 1990 1994

4

6

8

10

12

1974 1978 1982 1986 1990 1994

0.2

0.6

1.0

1.4

1974 1978 1982 1986 1990 1994

-5

0

5

10

15

20

1974 1978 1982 1986 1990 1994

0

0.4

0.8

1.2

1.6

1974 1978 1982 1986 1990 1994

45

50

55

60

65

70

Percent

Percent

Percent

Percent

Percent

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 7

Source: Bank AnnualSalomon Brothers, , 1992 and 1996 editions.

Figure 1.3

Bank Price-Earnings Ratios as a Percentage

of S&P 500 Price-Earnings Ratios,

1964–1995

Percent

1964

Note: Data for superregional bank price-earnings ratios begin in 1982.

1970 1975 1980 1985 1990 1995

40

50

60

70

80

90

100

Money-Center

Regional

Banks

Superregional

banks and were also well below the large-bank levels they would reach in the early 1990s.

Market data for large, publicly traded banking organizations suggest that investors were

valuing these institutions with reduced favor. During the 1960s and 1970s price-earnings

ratios for money-center banks trended generally downward relative to S&P 500 price-earn-

ings ratios, although for regional banks the decline was much less pronounced (see figure

1.3). For the 25 largest bank holding companies in the late 1970s and early 1980s, the mar-

ket value of capital decreased relative toand fell belowits book value, suggesting that

to investors, the franchise value of large banks was declining.

5

Differences in performance between large and small banks in 1980 are not surprising.

At that time, because of branching restrictions and deposit interest-rate controls, many

small institutions operated in still-protected markets. Accordingly, they were affected more

slowly by external forces such as increased competition and increased market volatility.

5

Michael C. Keeley, Deposit Insurance, Risk, and Market Power in Banking, American Economic Review (December

1990): 1185. Data are for the 25 largest bank holding companies as of 1985.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

8 History of the EightiesLessons for the Future

During the 1980s, of course, performance ratios of banks of all sizes weakened and exhib-

ited increased risk. Profitability declined and became more volatile, while loan charge-offs

rose dramatically.

6

Large banks assumed greater risk in order to boost profits, as is indicated

by the sharp rise in the ratio of loans and leases to total assets for these banks. In contrast,

equity ratios increased over the period, particularly for large banks, in line with increased

regulatory capital requirements and perhaps also in response to market concerns about dis-

tress in the banking system.

Then in the 1990s the performance of banking improved markedly. This is apparent

not only from the accounting data presented in figure 1.2 but also from the market data pre-

sented in figures 1.3 and 1.4, which suggest that to investors, the value of publicly traded

banks improved greatly in the 1990s. From 1993 to 1995, bank price-earnings ratios rose

relative to S&P 500 price-earnings ratios, although the movements in this measure were ex-

tremely volatile. After the early 1980s market prices per share of money-center and regional

banks increased from below book value per share to well above book value, except for a

sharp and temporary drop in 1990 (figure 1.4). The major improvement in the performance

and investor perceptions of banking in the 1990s, albeit of limited duration so far, does not

support earlier concerns that banking was a declining industry or the view that banking was

characterized by widespread and persistent overcapacity that would lead to increased fail-

ures.

7

Although the overall performance of the banking industry varied greatly during the

198094 period, in its structure the industry showed a strong trend in one directiontoward

consolidation into fewer banking organizations. This trend was partly due to the relaxation

of branching restrictions.

8

From the end of 1983 through the end of 1994, the number of in-

sured commercial banks declined by 28 percent, from 14,461 to 10,451. The number of

separate corporate unitsbank holding companies plus independent commercial banks

6

The 1986 peak in net loan charge-offs for small banks was associated with the agricultural, energy, and real estate problems

of the Southwest; the 1991 peak for large banks was associated with the real estate problems in the Northeast.

7

The issue of whether banking is a declining industry and the related question of overcapacity in banking are explored in Fed-

eral Reserve Bank of Chicago, The (Declining?) Role of Banking, Proceedings of the 30th Annual Conference on Bank

Structure and Competition (May 1994). In the Proceedings, see particularly Alan Greenspan, Optimal Bank Supervision

in a Changing World, 18; John H. Boyd and Mark Gertler, Are Banks Dead? Or, Are the Reports Greatly Exaggerated?

85117; and Sherrill Shaffer, Inferring Viability of the U.S. Banking Industry from Shifts in Conduct and Excess Capac-

ity, 130144. Shaffer concludes that a small amount of excess capacity in bank loans was eliminated in the mid-1980s.

8

Some observers have argued that bank failures in the 1980s were partly due to restrictions on bank ownership (geographic

restrictions within the banking industry, and prohibition of acquisitions by nonbank organizations), which prevented weak

or inefficient banks from being taken over before they failed. Although such restrictions on ownership probably contributed

to the rise in the number of bank failures, particularly in the early 1980s, the large number of voluntary mergers and con-

solidations within the industry may have averted some other failures by eliminating weaker institutions while they still had

some value.

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 9

Figure 1.4

Price-to-Book Value per Share,

1982–1995

Note: Values are industry composite medians. Data for superregional bank

price-to-book ratios begin in 1987.

Source: Bank AnnualSalomon Brothers, , 1992 and 1996 editions.

Money-Center

Regional

Banks

Superregional

Percent

1982 1984 1986 1988 1990 1992 1995

50

75

100

125

150

175

decreased somewhat more, by 31 percent. The 4,010 reduction in the number of insured

commercial banks was due primarily to the consolidation of bank affiliates of multibank

holding companies and to unassisted mergers of unaffiliated banks (4,803). The net effect

of failures, new charters, conversions, and other changes was an addition of 793 banks.

Legislative Developments

Banking legislation also played a large role in the bank-failure experience of the 1980s

and early 1990s.

9

This legislation was largely shaped by two broad factors: widespread

recognition that banking statutes should be modernized and adapted to new marketplace re-

alities, and the need to respond to the outbreak of bank and thrift failures. In the early 1980s

the focus was on the attempt to modernize, and congressional activity was dominated by ac-

tions to deregulate the product and service powers of thrifts and to a lesser extent of banks.

9

See Chapter 2, Banking Legislation and Regulation. Tax legislation was also a significant influence. After-tax yields on

real estate investment were enhanced by the Economic Recovery Act of 1981 and then reduced by the Tax Reform Act of

1986 (see the appendix to Chapter 3).

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

10 History of the EightiesLessons for the Future

These deregulatory actions were generally unaccompanied by actions to restrict the in-

creased risk taking they made possible, and so they contributed to bank and thrift failures.

As the number of failures mounted, the legislative emphasis then shifted to recapitalizing

the depleted deposit insurance funds and providing regulators with stronger tools, while at

the same time restricting their discretion. As a group, the various legislative actions ad-

dressed a variety of issues, but only the provisions most relevant to the increased number of

bank failures are discussed here.

The Depository Institutions Deregulation and Monetary Control Act of 1980

(DIDMCA) phased out deposit interest-rate ceilings, broadened the powers of thrift insti-

tutions, and raised the deposit insurance limit from $40,000 to $100,000. Two years later

the most pressing problem was the crisis of thrift institutions in an environment of high in-

terest rates. Accordingly, the GarnSt Germain Depository Institutions Act of 1982 (1)

authorized money market deposit accounts for banks and thrifts to stem disintermediation,

(2) authorized net worth certificates to implement capital forbearance for thrifts facing in-

solvency in the short term, and (3) increased the authority of thrifts to invest in commercial

loans to strengthen the institutions viability over the long term. In the case of national

banks, GarnSt Germain removed statutory restrictions on real estate lending, and relaxed

loans-to-one-borrower limits. With respect to commercial mortgage markets, this legisla-

tion set the stage for a rapid expansion of lending, an increase in competition between

thrifts and banks, overbuilding, and the subsequent commercial real estate market collapse

in many regions.

As the thrift crisis deepened and commercial bank problems were developing, Con-

gress passed the Competitive Equality Banking Act of 1987 (CEBA). It provided for re-

capitalizing the fund of the Federal Savings and Loan Insurance Corporation (FSLIC)

through the Financing Corporation (FICO), authorized a forbearance program for farm

banks, extended the full-faith-and-credit protection of the U.S. government to federally in-

sured deposits, and authorized bridge banks. Two years later, again grappling with the thrift

debacle, Congress passed the Financial Institutions Reform, Recovery, and Enforce-

ment Act of 1989 (FIRREA), which authorized the use of taxpayer funds to resolve failed

thrifts. Other provisions reflected congressional dissatisfaction with the regulation of

thrifts: the act abolished the existing thrift regulatory structure, moved thrift deposit insur-

ance to the FDIC, and mandated that bank and thrift insurance fund reserves be increased

to 1.25 percent of insured deposits.

The belief that regulators had not acted promptly to head off problems was again

evident in the Federal Deposit Insurance Corporation Improvement Act of 1991

(FDICIA). This act was aimed largely at limiting regulatory discretion in monitoring and

resolving industry problems. It prescribed a series of specific prompt corrective actions

to be taken as capital ratios of banks and thrifts declined to certain levels; mandated annual

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 11

10

Passage of the Deposit Insurance Funds Act was helped along by (1) the possibility of a FICO default if deposits were to

shift from the Savings Association Insurance Fund, with higher assessment rates, to the Bank Insurance Fund, with lower

assessment rates, and (2) the budgetary treatment of deposit insurance assessments, $3 billion of which was to be counted

as revenue to pay for nonbanking spending programs.

11

See Chapter 2, Banking Legislation and Regulation.

examinations and audits; prohibited the use of brokered deposits by undercapitalized insti-

tutions; restricted state bank activities; tightened least-cost standards for failure resolutions;

and mandated a risk-based deposit insurance assessment system.

Two years after the enactment of FDICIA, the Omnibus Budget Reconciliation Act

of 1993 included a national depositor preference provision, which provided that a failed

banks depositors (and the FDIC standing in the place of insured depositors it has already

paid) have priority over nondepositors claims. It was believed that national depositor pref-

erence would make failure transactions simpler and less expensive to the insurance fund

and would encourage nondeposit creditors to monitor bank risk more closely.

The final chapter of the savings and loan emergency legislation was completed in Oc-

tober 1996 with the enactment of the Deposit Insurance Funds Act, which provided for the

capitalization of the Savings Association Insurance Fund, phased in pro rata bank and thrift

payments of interest on FICO bonds, and required merger of the bank and thrift insurance

funds in 1999 if no savings associations are in existence at that time. Given Congresss past

reluctance to address promptly the need to fund thrift deposit insurance, enactment of this

legislation at a time when no major thrift failure was on the horizon suggests the extent to

which safety-and-soundness considerations had come to dominate banking legislation.

10

Legislation addressed not only the thrift and banking crises of the 1980s but also, af-

ter those crises had ended, the question of interstate banking. By the end of the 1980s the

risks posed by geographic lending concentrations were well understood, so attempts were

made to eliminate the remaining legal impediments to full interstate banking. Already state

action had enabled many banking firms to use bank holding company affiliations to cir-

cumvent geographic restrictions. Interstate banking was enacted in the Riegle-Neal Inter-

state Banking and Branching Efficiency Act of 1994, which enables banks to diversify

loan portfolios more effectively. (As noted below, it also requires existing regulatory risk-

monitoring systems to adapt to the changing nature of individual bank loan portfolios.)

Regulation

The tension between the two objectives of deregulating depository institutions and

preventing or containing failures was manifest not only in legislative activity but also in

policy differences among the federal bank regulators.

11

Of course, all three agencies were

sensitive to issues of safety and soundness as well as to the importance of modernizing bank

powers. On specific issues, however, the Office of the Comptroller of the Currency (OCC)

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

12 History of the EightiesLessons for the Future

12

With respect to the potential short-term conflict between pro-competitive and safety-and-soundness objectives, the fol-

lowing statement on S&L deregulation, made by the National Commission on Financial Institution Reform, Recovery and

Enforcement, is instructive: [C]ommon sense and prudence should have dictated that the industry be required to wait out

the high interest rates, regain net worth, and then gradually shift into new activities. This is what well-managed and re-

sponsible S&Ls did on their own, and they were largely successful (Origins and Causes of the S&L Debacle: A Blueprint

for Reform [1993], 32).

13

In 1984, 356 new commercial banks were chartered. By 1994 the number had declined to 47, but it then increased to 97 in

1995 and 140 in 1996.

tended to emphasize the need to allow banks more freedom to compete and seek profit op-

portunities, the FDIC leaned toward protecting the deposit insurance fund, and the Federal

Reserve often took a middle-of-the-road position.

Differences between the FDIC and the OCC reflected the different responsibilities of

an insurer and a chartering agency. They also reflected a problem that may potentially arise

in bank regulation regardless of the agency involved: how to strike the correct balance be-

tween encouraging increased competition and preserving stability and safety. To be sure, no

such conflict is likely to exist in the long run: depository institutions must be able to com-

pete and to participate in market innovations if they are to be viable in the long term. At any

particular time, however, a short-term conflict may arise. The classic case is that of the sav-

ings and loan industry. Broadened nonmortgage powers were deemed essential to the long-

term viability of thrift institutions, but the very act of providing these powers (without

appropriate safeguards and at a time when thrifts were undercapitalized) contributed to the

collapse of many thrift institutions and the weakening of many banks in the 1980s.

12

In varying degree, differences among regulators were evident in the development of

policies relating to chartering new banks, the use of brokered funds, and capital require-

ments. With respect to the entry of new banks, both the OCC and the states sharply in-

creased chartering in the 1980s. (Texaswhere branching was restrictedaccounted for

particularly large shares of total new state and national bank charters.) In 1980, when the

OCC sought to foster increased competition by allowing new entrants into banking mar-

kets, the agency revised its requirements for approving new charters. But when a dispro-

portionate number of new banks became troubled and failed, the FDIC expressed its

concern about the OCCs policy. A basic issue was the FDICs ability to deny insurance

coverage to newly chartered institutions. FDIC approval of insurance was, for all practical

purposes, necessary before a state would grant a new charter, but national banks and Fed-

eral Reserve member banks received insurance upon being chartered as a matter of law.

Congress settled this issue in FDICIA by requiring that all institutions seeking insurance

formally apply to the FDIC, thereby assuring the deposit insurer a role in new bank char-

tering. Meanwhile, the number of new commercial bank charters reached a peak in 1984,

then gradually declined until 1994.

13

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 13

The regulators also differed on the appropriate treatment of brokered deposits. (Bro-

kered deposits had a largely indirect influence on bank failures in that many weak savings

institutions used them to fund rapid loan expansion in competition with healthier banks and

thrift institutions.) In 1984, the FDIC and the Federal Home Loan Bank Board proposed

that brokered deposits be insured only up to $100,000 per broker per bank, whereas the

OCC favored a less-stringent approach. Safety-and-soundness considerations seemed to be

pitted against the objective of permitting evolution to proceed in the financial markets. In

the end Congress stepped in, and both FIRREA and FDICIA limited the use of brokered de-

posits by troubled institutions.

A third instance of regulatory disagreement concerned the adoption of formal capital

requirements with uniform standards for minimum capital levels. In view of the relatively

low capital ratios at many large banks and the rise in the number of failures, all of the agen-

cies favored the objective of explicit capital standards, but initially they differed on the

specifics; the FDIC generally favored higher capital requirements than the OCC, and the

Federal Reserve offered a compromise in at least one instance. In 1985, with congressional

encouragement, the regulators agreed on a uniform system covering all banks. In 1990 a

further, major change came with the adoption of interim risk-based capital requirements,

supplemented by leverage requirements. Capital standards became part of the triggering

mechanism for the Prompt Corrective Action (PCA) prescribed by FDICIA in 1991. Final

risk-based requirements took effect in 1992.

Geographic Pattern of Bank Failures

The national economic, legislative, and regulatory factors discussed above affected

potentially all banks. A variety of other factors affected banks differently in particular

regions of the country, as indicated by the geographic pattern of bank failures. During

the 198094 period, 1,617 FDIC-insured commercial and savings banks were closed or

received FDIC financial assistance (see table 1.1). This number was 9.14 percent of the sum

of all banks existing at the end of 1979 plus all banks chartered during the subsequent

15 years. The comparable figure for the preceding 15-year period (196579) was 0.3

percent.

The geographic pattern of bank failures can be expressed in a number of waysby

number of failed banks, amount of failed-bank assets, proportion of failed banks and failed-

bank assets relative to all banks in individual states, or particular states shares in national

totals for bank failures and failed-bank assets. But by any of these measures, it is evident

that bank failures during the 198094 period were highly concentrated in relatively few re-

gionswhich, however, included some of the countrys largest banking markets in terms of

number of institutions and dollar resources. Thus, geographically confined crises were

translated into a national problem. At one end of the scale, in 7 states the number of bank

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

14 History of the EightiesLessons for the Future

Table 1.1

Bank Failures by State, 19801994

Number of Bank Percent of Total Assets of Failed Banks Percent of Total

Failures Number of Banks ($Thousands) Bank Assets

Alabama 9 2.47 $ 215,589 1.18

Alaska 8 44.44 1,083,417 41.58

Arizona 17 26.15 331,059 1.66

Arkansas 11 4.03 160,797 1.47

California 87 15.26 4,222,302 1.69

Colorado 59 12.39 1,035,553 5.24

Connecticut 32 18.39 6,818,223 22.17

Delaware 1 1.61 582,350 0.74

District of Columbia 5 17.86 1,135,066 13.39

Florida 39 4.56 4,524,461 4.30

Georgia 3 0.53 60,922 0.17

Hawaii 2 20.00 13,941 0.29

Idaho 1 3.13 42,931 0.84

Illinois 33 2.52 35,031,196 25.75

Indiana 10 2.40 241,463 0.76

Iowa 40 6.07 652,681 3.25

Kansas 69 10.71 1,233,874 7.26

Kentucky 7 1.91 97,742 0.48

Louisiana 70 22.44 4,105,621 17.39

Maine 2 2.63 875,303 13.51

Maryland 2 1.45 43,827 0.06

Massachusetts 44 10.63 10,240,719 12.90

Michigan 3 0.75 159,917 0.29

Minnesota 38 4.87 1,491,250 4.95

Mississippi 3 1.63 338,680 3.18

Missouri 41 5.24 1,043,379 2.25

Montana 10 5.75 172,739 3.32

Nebraska 33 6.88 323,646 2.91

Nevada 1 4.17 18,036 0.10

New Hampshire 16 12.60 3,320,916 31.98

New Jersey 14 5.71 4,695,156 9.49

New Mexico 11 11.00 568,326 9.47

New York 34 8.79 31,701,442 6.22

North Carolina 2 1.59 74,553 0.27

North Dakota 9 5.00 77,565 1.76

Ohio 5 1.14 171,765 0.29

Oklahoma 122 22.02 5,838,273 23.85

Oregon 17 17.00 599,703 4.34

Pennsylvania 5 1.19 17,454,150 16.99

Puerto Rico 5 33.33 527,375 8.94

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 15

Table 1.1 (continued)

Bank Failures by State, 19801994

Number of Bank Percent of Total Assets of Failed Banks Percent of Total

Failures Number of Banks ($Thousands) Bank Assets

Rhode Island 2 8.33 323,861 3.29

South Carolina 1 0.87 64,629 0.67

South Dakota 8 4.73 711,345 4.04

Tennessee 36 9.05 1,730,076 6.34

Texas 599 29.41 60,192,424 43.84

Utah 11 11.58 339,237 4.04

Vermont 2 5.41 93,802 2.94

Virginia 7 2.45 133,529 0.47

Washington 4 2.63 713,803 2.42

West Virginia 5 1.98 123,829 1.25

Wisconsin 2 0.30 50,882 0.19

Wyoming 20 16.67 375,332 10.30

U.S. 1,617 9.14% $206,178,657 8.98%

Note: Data refer to FDIC-insured commercial and savings banks that were closed or received FDIC assistance. Total num-

ber of banks is the number of banks on December 31, 1979, plus banks newly chartered in 198094. Asset data are assets of

banks existing on December 31, 1979, plus assets of newly chartered banks as of date of failure, merger, or December 31,

1994, whichever is applicable, and first available assets for Massachusetts banks that became FDIC-insured in the mid-1980s.

Data exclude 13 newly chartered banks that reported no asset figures and 4 banks in U.S. territories.

14

The 8.98 percent figure refers to the failed-bank portion of the following: assets of all banks existing as of December 31,

1979, plus assets of banks chartered in 198094 as of the date of merger, failure, or December 31, 1994, whichever is ap-

plicable, and first available assets for Massachusetts banks that became FDIC-insured in the mid-1980s. Data are not ad-

justed for inflation.

failures constituted at least 20 percent of the total number of existing and new banks

(Alaska, Arizona, Hawaii, Louisiana, Oklahoma, Puerto Rico, and Texas). At the other end

of the scale, in 24 states bank failures represented less than 5 percent of the total number of

existing and new banks. Of the total 1,617 failures during the entire 198094 period, nearly

60 percent were in only 5 states: California, Kansas, Louisiana, Oklahoma, and Texas.

Included in these numbers are failures of bank holding company subsidiaries; in Texas and

other states with branching restrictions, these were more like branches than independent

institutions.

An alternative measure of the severity of bank failures is based on assets. Assets of

banks failing in 198094 constituted 8.98 percent of the sum of total bank assets at the end

of 1979 plus the assets of banks chartered during the 198094 period.

14

In 6 states (Alaska,

Connecticut, Illinois, New Hampshire, Oklahoma, and Texas), failed-bank assets consti-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

16 History of the EightiesLessons for the Future

tuted at least 20 percent of total assets at year-end 1979 plus new-bank assets. On the other

hand, in 33 states the failed-bank share was less than 5 percent. Of all banks that failed dur-

ing the 198094 period, 59 percent of assets at the quarter before failure were accounted for

by 3 states: Illinois, New York, and Texas. (See table 1.2.)

15

Although widespread bank failures were limited to a few areas of the country, even a

relatively small number of failures could cause serious strains on the deposit insurance

fund. In 1988, for example, the number of failures and the amount of failed-bank assets

reached post-Depression records of 279 and $54 billion (nominal dollars), respectively, but

still represented in each case less than 2 percent of the total number of banks and total bank

assets at the beginning of the year. Nevertheless, in that year the FDIC sustained the first

operating loss in its history, and operating losses continued through 1991, after which, pro-

visions for insurance losses were sharply reduced. And even the smaller number of failures

before 1988 had an evident effect on the FDICs income and expense position. Beginning

in 1984, provisions for insurance losses exceeded annual deposit insurance assessments,

and this shortfall continued through 1990.

16

The figures by state illustrate some of the factors associated with bank failures. The

incidence of failure was particularly high in states characterized by

severe economic downturns related to the collapse in energy prices (Alaska, Louisiana,

Oklahoma, Texas, and Wyoming);

real estaterelated downturns (California, the Northeast, and the Southwest);

the agricultural recession of the early 1980s (Iowa, Kansas, Nebraska, Oklahoma, and

Texas);

an influx of banks chartered in the 1980s (California and Texas) and the parallel phe-

nomenon of mutual-to-stock conversions (Massachusetts);

prohibitions against branching that limited banks ability to diversify their loan portfo-

lios geographically and to fund growth through core deposits (Colorado, Illinois,

Kansas, Texas, and Wyoming);

17

the failure of a single large bank (Illinois) or of a small number of relatively large banks

(New York and Pennsylvania).

15

Comparisons based on assets of failed banks are subject to distortion because of the effect of inflation, differences in the

timing of failures among the states, and differences in asset dates between new banks and banks existing at year-end 1979.

16

Beginning in 1989, data refer to the Bank Insurance Fund (FDIC, Annual Report, various years).

17

Information on state branching provisions is as of September 30, 1985, as compiled by the Conference of State Bank Su-

pervisors. CSBS listed 7 states as having unit banking as of September 30, 1985, 6 as a result of legal prohibitions (Col-

orado, Illinois, Kansas, Montana, North Dakota, and Texas). One (Wyoming) had no statute, but unit banking was

prevalent.

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 17

Table 1.2

Assets of Failed Banks at the Quarter before Failure, by State, 19801994

Assets of Failed Banks

State ($Thousands) Percent Distribution

Alabama $ 266,443 0.08

Alaska 3,049,573 0.96

Arizona 453,522 0.14

Arkansas 229,700 0.07

California 6,018,036 1.90

Colorado 1,072,556 0.34

Connecticut 17,717,959 5.59

Delaware 582,350 0.18

District of Columbia 2,189,658 0.69

Florida 15,471,515 4.88

Georgia 104,607 0.03

Hawaii 11,486 0.00

Idaho 55,867 0.02

Illinois 40,765,430 12.87

Indiana 311,825 0.10

Iowa 809,089 0.26

Kansas 1,697,588 0.54

Kentucky 114,931 0.04

Louisiana 4,616,370 1.46

Maine 2,228,177 0.70

Maryland 57,000 0.02

Massachusetts 26,632,401 8.41

Michigan 160,300 0.05

Minnesota 1,669,974 0.53

Mississippi 288,949 0.09

Missouri 3,096,719 0.98

Montana 212,896 0.07

Nebraska 402,185 0.13

Nevada 18,036 0.01

New Hampshire 5,393,842 1.70

New Jersey 6,919,198 2.18

New Mexico 723,576 0.23

New York 51,577,291 16.28

North Carolina 74,553 0.02

North Dakota 120,109 0.04

Ohio 152,254 0.05

Oklahoma 6,712,651 2.12

Oregon 622,091 0.20

Pennsylvania 14,265,742 4.50

(continued)

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

18 History of the EightiesLessons for the Future

Table 1.2 (continued)

Assets of Failed Banks at the Quarter before Failure, by State, 19801994

Assets of Failed Banks

State ($Thousands) Percent Distribution

Puerto Rico 543,748 0.17

Rhode Island 600,706 0.19

South Carolina 64,629 0.02

South Dakota 743,698 0.23

Tennessee 2,446,083 0.77

Texas 93,061,510 29.37

Utah 469,637 0.15

Vermont 329,478 0.10

Virginia 296,368 0.09

Washington 769,109 0.24

West Virginia 123,139 0.04

Wisconsin 70,757 0.02

Wyoming 428,606 0.14

U.S. $316,813,917 100.00%

Note: Failed-bank assets are assets as of the quarter before failure or assistance, or assets as of the last available Call Report

before failure or assistance.

In some states bank failures were affected by more than one of these factors. For ex-

ample, the particularly high incidence of failures in Texas reflected the rapid rise and sub-

sequent collapse in oil prices, the commercial real estate boom and bust, the effects of the

agricultural recession, the large number of new banks chartered in the state during the

1980s, and state prohibitions against branching. (The high proportion of bank failures in

Texas also reflected supervisory developments. As noted below, declines in the number and

frequency of on-site examinations in the 198386 period were particularly pronounced in

Texas; earlier identification of troubled banks might have prevented some failures.)

18

By

the same token, some states that exhibited only one or two of the factors associated with

bank failures had relatively few failures. Montana and North Dakota, for example, had pro-

hibitions against branching, but their failure rates were below the national average, whether

measured by number of institutions or by assets. Differences among the states in failure

rates and in the presence or absence of factors associated with failures illustrate the conclu-

sion that the rise in the number of bank failures cannot be ascribed to any single cause.

18

Texas was also a leading state for S&L failures. Texas S&Ls accounted for 18 percent of all of the failures resolved by the

Resolution Trust Corporation (RTC), 14 percent of S&L assets at time of takeover, and 29 percent of total estimated RTC

resolution costs. See RTC, Statistical Abstract (August 1989/September 1995).

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 19

Regional and Sectoral Recessions

Although the interplay of broad economic, legislative, and regulatory forces helped

make the environment for banking increasingly demanding, the more immediate cause of

bank failures was a series of regional and sectoral recessions. Because most U.S. banks

served relatively narrow geographic markets, these regional and sectoral recessions had a

severe impact on local banks. It should be noted, however, that not all regional recessions

of the magnitude experienced during the 198094 period resulted in a major increase in the

number of bank failures. Rather, bank failures were generally associated with regional re-

cessions that had been preceded by rapid regional expansionsthat is, they were associated

with boom-and-bust patterns of economic activity. Bank loans helped to fuel the boom

phase of the cycle, and when economic activity turned down, some of these loans went sour,

with the result that banks holding these loans were weakened. By contrast, recessions that

were preceded by relatively slow economic activity, such as those in the Rust Belt, gener-

ally did not lead to widespread bank failures.

This relationship between the number of bank failures and regional boom-and-bust

patterns of economic activity is illustrated by the data in tables 1.3 and 1.4, which show that

bank failure rates were generally high in states where, in the five years preceding state re-

cessions, real personal income grew faster than it did for the nation as a whole. Conversely,

bank failure rates were relatively low in states where, in the five years preceding state re-

cessions, real personal income grew more slowly than it did for the nation as a whole.

19

There were four major regional and sectoral economic recessions that were associated

with widespread bank failures during the 198094 period. The first accompanied the down-

turn in farm prices in the early and middle 1980s after years of rapid increases during the

late 1970s (see figure 1.5). The downturn in prices led to reductions in net farm income and

farm real estate values and a rise in the number of failures of banks with heavy concentra-

tions of agricultural loans. The second recession occurred in Texas and other energy-

producing southwestern states, where gross state product dropped after oil prices turned

down in 1981 and again in 1985 (see figure 1.6). The 1981 oil price reduction was followed

by a regional boom and bust in commercial real estate activity. The third recession was in

the northeastern states, which experienced negative growth in gross state product in

199091. The final episode was a recession in California, as growth in gross state product

turned negative in 199192.

Of the 1,617 bank failure and assistance cases from 1980 to 1994, 78 percent were lo-

cated in the regions suffering these economic downturnsthe Southwest, the Northeast,

19

In some high-growth states the number of bank failures rose sharply after the states recessions, but the increase fell out-

side the three-year periods shown in table 1.3. For example, Arizona experienced especially rapid growth before the states

1982 recession and also saw a high rate of bank failures (tables 1.1 and 1.2), but most of them occurred in 198990.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

20 History of the EightiesLessons for the Future

Table 1.3

Bank Failures and Growth Rates of Real Personal Income, by State,

19801994 (Percent)

Growth Rates of Real Personal Income

Five Years before Recession

State Minus Percent of Banks Failing

Recession State Growth Rate, State Growth U.S. Growth in Recession and Next 2

State* Years Recession Years Rate Rate Years

Wyoming 198287 −3.03 8.26 5.05 18.52

Nevada 1982 −0.17 7.83 4.62 8.33

Oklahoma 198387 −1.42 6.05 3.78 20.83

Alaska 198687 −5.46 6.63 3.75 50.00

Arizona 1982 −0.18 6.69 3.49 0.00

New Hampshire 199091 −0.43 5.69 2.50 19.51

Louisiana 198387 −0.75 4.69 2.41 21.22

Washington 1982 −0.24 4.97 1.76 0.93

Maryland 1991 −0.33 4.49 1.61 1.92

Texas 198687 −0.98 4.43 1.55 20.45

Maine 1991 −2.15 4.42 1.54 5.13

Vermont 1991 −1.45 4.32 1.44 6.25

Connecticut 1991 −1.94 4.30 1.42 22.05

California 1991 −1.04 4.20 1.32 7.26

Oregon 198182 −2.40 5.03 1.21 14.63

New Jersey 1991 −1.13 3.89 1.01 6.00

Rhode Island 1991 −1.82 3.79 0.91 13.33

Massachusetts 1991 −1.87 3.79 0.91 9.77

New York 1991 −0.88 3.71 0.83 3.86

Mississippi 1980 −1.09 4.15 0.42 0.00

Arkansas 198082 0.27 4.14 0.42 2.33

Kentucky 198083 0.17 4.08 0.36 0.58

Tennessee 1982 −0.05 3.12 −0.09 7.41

West Virginia 198183 −0.73 3.63 −0.19 0.84

Illinois 1991 −0.09 2.64 −0.24 0.55

Missouri 198082 0.55 3.41 −0.32 0.69

Wisconsin 198182 −0.22 3.49 −0.33 0.00

North Dakota 198588 −3.54 2.28 −0.38 4.52

Kansas 1980 −0.30 3.32 −0.41 0.49

Idaho 1982 −1.91 2.79 −0.41 0.00

Michigan 1991 −0.58 2.41 −0.47 0.00

Alabama 1982 −0.24 2.72 −0.48 0.97

Michigan 198082 −2.73 3.12 −0.60 0.54

Hawaii 1981 −0.63 3.20 −0.62 0.00

Indiana 198082 −1.39 3.03 −0.69 0.49

Iowa 197985 −0.31 1.83 −0.79 4.92

Iowa 1991 −0.39 2.04 −0.84 0.18

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 21

Table 1.3 (continued)

Bank Failures and Growth Rates of Real Personal Income, by State,

19801994 (Percent)

Growth Rates of Real Personal Income

Five Years before Recession

State Minus Percent of Banks Failing

Recession State Growth Rate, State Growth U.S. Growth in Recession and Next 2

State* Years Recession Years Rate Rate Years

Montana 198082 1.21 2.87 −0.86 0.62

Nebraska 197983 0.24 1.67 −0.96 4.20

Montana 198588 −0.17 1.39 −1.28 4.79

Ohio 198082 −0.73 2.41 −1.31 0.00

Illinois 198082 −0.28 2.34 −1.38 1.60

South Dakota 198082 −1.38 2.09 −1.63 1.30

West Virginia 1987 −1.33 0.51 −2.65 0.47

North Dakota 1991 −2.50 0.08 −2.80 0.00

Iowa 1988 −1.11 1.01 −3.09 1.17

District of Columbia 1980 −2.94 −0.08 −3.80 0.00

North Dakota 197980 −3.54 −1.59 −4.21 0.58

Note: Data refer to all states that experienced a decrease in real personal income in any year from 1980 to 1992.

*States are ranked according to the magnitude of the difference between state growth rates and the U.S. growth rate in real

personal income during the five years before state recessions.

Recessions are defined as years in which personal income deflated by GDP deflator decreased. Recoveries are counted as

having at least two consecutive years of growth in real personal income. In some states, therefore, personal income increased

during a single year sufficiently to produce positive growth for the recession as a whole.

Percent of banks failing is based on the number of banks existing as of December of the year preceding the recession.

Table 1.4

Bank Failures and Growth Rates of Real Personal Income,

by State Recession Quartile

(Percent)

Average Difference between State Average State Bank Failure

State Recession Growth Rate and U.S. Growth Rate, Rate in Recession

Quartile* 5 Years before Recession and Next 2 Years

1 2.79 14.42

2 0.71 7.34

3 −0.48 1.06

4 −2.07 1.28

*State recessions are grouped in quartiles according to the magnitude of the difference between state growth rate and U.S.

growth rate in real personal income from table 1.3.

Data are unweighted averages of individual state data.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

22 History of the EightiesLessons for the Future

$Billions

$Billions

Index

$Billions

Average Farm Real Estate Value per Acre

Farm Debt

Source: Economic Report of the President, 1986, 1996.

Figure 1.5

Farm Prices, Exports, Income, Debt, and Real Estate Value, 1975 94–19

Farm Exports

Prices Received by Farmers

Net Farm Income

Dollars

1990 1992 = 100–

1975 1980 1985 1990 1994

25

35

45

1975 1980 1985 1990 1994

20

30

40

1975 1980 1985 1990 1994

90

120

150

180

1975 1980 1985 1990 1994

80

90

100

1975 1980 1985 1990 1994

400

600

800

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 23

Figure 1.6

Changes in Gross State Product and Gross Domestic Product, 1980–1994

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

California

NortheastSouthwest

Peak Number

of Failures

Peak Number

of Failures

Peak Number

of Failures

Percent

Percent

Percent

1980 1982 1984 1986 1988 1990 1992 1994

-3

0

3

6

9

1980 1982 1984 1986 1988 1990 1992 1994

-3

0

3

6

9

1980 1982 1984 1986 1988 1990 1992 1994

-3

0

3

6

9

U.S.

U.S.

U.S.

Southwest

Northeast

California

and Californiaor were agricultural banks outside of these three regions.

20

These failures

accounted for 71 percent of the assets of failed banks over the period. Although all four of

20

Agricultural banks are defined as banks with 25 percent or more of total loans in agricultural loans. Data on assets of failed

banks are as of the quarter before the date of failure. The Southwest includes Arkansas, Louisiana, New Mexico, Okla-

homa, and Texas. The Northeast includes New Jersey, New York, and the six New England states (Connecticut, Maine,

Massachusetts, New Hampshire, Rhode Island, and Vermont). The bulk of the agricultural bank failures, other than those

in the two southwestern states of Oklahoma and Texas, were in Iowa, Kansas, Minnesota, Missouri, and Nebraska.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

24 History of the EightiesLessons for the Future

21

See Chapter 8, Banking and the Agricultural Problems of the 1980s.

22

See John OKeefe, The Texas Banking Crisis: Causes and Consequences, 19801989, FDIC Banking Review 3, no. 2

(1990); and Chapter 9, Banking Problems in the Southwest.

23

See Chapter 11, Banking Problems in California.

24

See Chapter 10, Banking Problems in the Northeast.

the recessions associated with bank failures were partly shaped by their own distinct cir-

cumstances, certain common elements were present:

1. Each followed a period of rapid expansion; in most cases, cyclical forces were ac-

centuated by external factors.

2. In all four recessions, speculative activity was evident. Expert opinion often

gave support to overly optimistic expectations.

3. In all four cases there were wide swings in real estate activity, and these con-

tributed to the severity of the regional recessions.

4. Commercial real estate markets in particular deserve attention because boom and

bust activity in these markets was one of the main causes of losses at both failed

and surviving banks.

Rapid expansion. In the agricultural belt, increased farm production and purchases of

farmland were stimulated by rapid inflation during the 1970s in the prices of farm products,

a sharp run-up in farm exports, and widespread expectations of strong worldwide demand

in the 1980s. But as farm exports declined and higher interest rates increased farm costs, the

expansion gave way to a downturn.

21

Similarly, in the Southwest (as well as other oil-pro-

ducing areas around the world) strong worldwide demand for oil plus OPEC restrictions on

supply led to a major rise in oil prices and strong economic expansionbut the weakening

in oil prices after 1981 and their rapid drop in 1985 (brought on partly by the collapse of dis-

cipline in the international oil cartel) resulted in two economic downturns during the 1980s

in the Southwest.

22

California enjoyed a rate of economic growth above the national aver-

age during the 1980s but was hit particularly hard during the 199192 national recession,

partly because of cutbacks in defense spending.

23

In the Northeast, growth rates in overall

production were above the national average during 198288; the subsequent decline came

about mainly because a local economic slowdown was followedand aggravatedby the

199192 national economic recession and by a boom and bust in northeastern residential

and commercial real estate activity.

24

Speculative activity with expert support. Speculative activity was reflected in a

number of developments. Farm real estate values showed an uninterrupted rise in the late

1970s and early 1980s, even though gross returns per acre for major crops were tracing a

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 25

25

In 1982, when land values reached their zenith, gross rates of return for corn and soybeans were less than two-thirds their

1970 levels and approximately one-third their 1973 levels. See Chapter 8, Banking and the Agricultural Problems of the

1980s.

26

See Chapter 3, Commercial Real Estate and the Banking Crises; and OKeefe, The Texas Banking Crisis.

27

Speculative activity in this context is synonymous with economic bubbles defined as follows: if the reason that the

price is high today is only because investors believe that the selling price will be high tomorrowwhen fundamental fac-

tors do not seem to justify such a pricethen a bubble exists. See Joseph E. Stiglitz, Symposium on Bubbles, Journal

of Economic Perspectives 4, no. 2 (spring 1990): 13.

28

Robert Bergland, secretary of agriculture in 1980, said, The era of chronic overproduction...is over. In 1972, then-Secre-

tary of Agriculture Earl Butz is said to have advised farmers to plant from fencerow to fencerow. (Both quotations are

from Gregg Easterbrook, Making Sense of Agriculture: A Revisionist Look at Farm Policy, The Atlantic 256 (July 1985):

63. See Chapter 8, Banking and the Agricultural Problems of the 1980s.

29

Interviews with regulators and bankers. See Chapter 10, Banking Problems in the Northeast.

30

See citations in Chapter 11, Banking Problems in California.

highly variable and generally downward trend.

25

In the Southwest, commercial construc-

tion and lending activity continued in major markets after vacancy rates began to soar. In

many commercial real estate mortgage markets, underwriting standards were relaxed.

26

The

presence of speculative activity was frequently mentioned in interviews conducted in 1995

by staff of the FDICs Division of Research and Statistics as part of the research for this

study.

27

(In all, approximately 150 bankers and regulators were interviewed in Atlanta,

Boston, Dallas, Kansas City, New York, San Francisco, and Washington). Numerous inter-

viewees cited a belief common in the 1980s that the boom economies of this period had un-

limited viability. They also noted that in many cases bankers were engaged in asset-based

lending, relying on collateral values supported by inflationary expectations rather than by

cash flows.

Examples of expert opinion that supported optimism included statements attributed

to two secretaries of agriculture

28

and comments by many observers in the Northeast that

the areas economy was diversified, mature, and largely immune to Texas-style real estate

problems.

29

Another example is provided by economists and other analysts, who as late as

1990 and 1991 were discounting the prospect of a bust in California home prices.

30

Wide swings in real estate activity. In the agricultural belt, prices of farmland were bid

up during the 1970s by farmers and investors, who were responding to increases in the

prices of farm products as well as expectations of continued strong foreign demand. Farm-

land values continued to rise until 1982, remained at high levels until 1984, and then col-

lapsed (figure 1.5). In the Southwest, both residential and nonresidential construction rose

sharply during the early 1980s before falling precipitously later in the decade; these wide

real estate swings followed the earlier oil-generated cycle and contributed to the second

Southwest recession in the 1980s. In both the northeastern states and California, boom-and-

bust real estate activity aggravated general state recessions in the early 1990s.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

26 History of the EightiesLessons for the Future

Commercial real estate markets and bank losses. Commercial real estate development

is inherently risky, partly because of the long gestation period of many commercial con-

struction projects. When completed projects finally come to market, demand conditions

may have changed considerably from what they were at the time of conception. Another

cause of risk is that many firms seeking commercial floor space are geographically mobile,

so developers are affected by economic events not only in the projects proximity but in far-

distant areas as well. In addition, commercial real estate projects tend to be highly lever-

aged, a condition that increases the volatility of returns. Relevant data on commercial real

estate are often difficult to obtain because these markets are not highly organized and be-

cause transactions are often private deals whose crucial elements may not be publicly

available. Finally, commercial loan contracts usually have nonrecourse provisions prohibit-

ing lenders from satisfying losses from other borrower assets.

In the early 1980s, booming activity in commercial construction was supported by

rapidly increased bank and thrift commercial mortgage lending. A major stimulus for this

activity was provided by public policy actions: tax breaks enacted as part of the Economic

Recovery Act of 1981 greatly enhanced the after-tax returns on real estate investment, and

the GarnSt Germain Act expanded the nonresidential lending powers of savings associa-

tions. Competitive pressures, including those reflected in the reduced bank share of the

market for business loans to large companies, also provided an important stimulus.

Many banks and thrifts moved aggressively into commercial real estate lending. Dur-

ing the 1980s, when total real estate loans of banks more than tripled, commercial real es-

tate loans nearly quadrupled. As a percentage of total bank assets, total real estate loans rose

from 18 to 27 percent between 1980 and 1990, while the ratio for nonresidential and con-

struction loans nearly doubled, from 6 to 11 percent. A pervasive relaxation of underwriting

standards took place, unchecked either by the real estate appraisal system or by supervisory

restraints. Overly optimistic appraisals, together with the relaxation of debt coverage, of

maximum loan-to-value ratios, and of other underwriting constraints, meant that borrowers

frequently had no equity at stake, and lenders bore all of the risk.

31

Overbuilding occurred in many markets, and when the bubble burst, real estate values

collapsed. (The downturn was aggravated by the Tax Reform Act of 1986, which removed

tax breaks for real estate investment and caused a reduction in after-tax returns on such in-

vestment.) At many financial institutions loan quality deteriorated significantly, and the de-

terioration caused serious problems. As discussed in detail below, banks that failed in the

1980s had higher ratios of commercial real estate loans to total assets than surviving banks.

31

These observations on underwriting practices, taken from Chapter 3, reflect the comments of, and have been reviewed by,

a number of FDIC examiners and supervisory personnel who were actively engaged in bank examination and supervision

during the 1980s.

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 27

Failing banks also had higher ratios of commercial real estate loans to total real estate loans,

of real estate charge-offs to total charge-offs, and of nonperforming real estate assets to to-

tal nonperforming assets.

Bank Performance in Regional and Sectoral Recessions

The behavior of banks in the regions and sectors that suffered recessions during the

1980s also exhibited some common elements:

1. In the economic expansions that preceded these recessions, banks generally responded

aggressively to rising credit demands.

2. Banks that failed during the regional recessions generally had assumed greater risks, on

average, than those that survived, as measured by ratios of total loans and commercial

real estate loans to total assets. Banks that failed had generally not been in a seriously

weak condition (as measured by equity-to-assets ratios) in the years preceding the re-

gional recessions.

3. Banks chartered in the 1980s and mutual institutions converting to the stock form of

ownership failed with greater frequency than comparable banks.

Aggressive response. In the case of agricultural banks, aggressive response is evident

in the growth of farm loans, which increased rapidly and reached a peak in 1984, after the

1981 highs in prices received by farmers and net farm income and the 1982 high in farm-

land values. In Texas, banks responded to the rise in oil prices by rapidly increasing not only

their commercial and industrial loans (including loans to oil and gas producers) but also the

share of commercial and industrial loans in total bank assets. In most of the regions that un-

derwent recessions, the aggressiveness of bank lending is evident as well in the rapid ex-

pansion in nonresidential mortgage lending and in the increased share of commercial

mortgages in total bank assets.

Risk taking and failure. Banks that would fail during the 198094 period generally had

higher ratios of total loans to assets and commercial real estate loans to assets throughout

most of the period (see figures 1.7 and 1.8). (In this context, commercial real estate loans in-

clude construction loans, nonfarm nonresidential loans, and multifamily mortgages.) This

was true for banks in the agricultural belt, the Southwest, the Northeast, California, and the

total United States. In the agricultural belt, the Southwest, and the Northeast, banks that

would fail during the regional recessions had significantly higher loans-to-assets ratios in

the year before the recessions began (see table 1.5).

32

In the Northeast and Southwest, com-

32

Regional recessions are considered to have begun in the agricultural belt in 1982 (following the 1981 high in prices re-

ceived by farmers), in the Southwest in 1982 (after oil prices reached a peak in 1981), and in the Northeast and California

in the first year of negative gross state product (figure 1.6).

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

28 History of the EightiesLessons for the Future

Percent

Percent

Percent

Percent

Total U.S.

California

Figure 1.7

Ratio of Gross Loans to Total Assets, Failed and Nonfailed Banks, 1980 94–19

Southwest

Northeast

Percent

Agricultural Banks*

Note: Data are unweighted averages of individual bank ratios. Data for banks that subsequently failed are not shown for years when

there were fewer than ten banks that would fail in subsequent years. Open-bank assistance cases are not counted as failures.

Banks That Subsequently Failed

Banks That Did Not Fail

Agricultural banks are banks where agricultural loans are at least

25% of total loans.

1980 1982 1984 1986 1988 1990 1992 1994

45

*

50

55

60

1980 1982 1984 1986 1988 1990 1992 1994

45

55

65

1980 1982 1984 1986 1988 1990 1992 1994

55

65

75

1980 1982 1984 1986 1988 1990 1992 1994

55

65

75

1980 1982 1984 1986 1988 1990 1992 1994

50

60

70

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 29

Percent

1980 1982 1984 1986 1988 1990 1992 1994

0

10

20

30

Percent

Percent

Percent

Percent

Total U.S.

California

Figure 1.8

Ratio of Commercial Real Estate Loans to Total Assets, Failed

and Nonfailed Banks, 1980 94–19

Southwest

Northeast

Agricultural Banks*

Note: Commercial real estate loans = construction loans + multifamily loans + nonfarm, nonresidential loans. Data are

unweighted averages of individual bank ratios of commercial real estate loans to total assets. Data for banks that subsequently

failed are not shown for years when there were fewer than ten banks that would fail in subsequent years. Open-bank assistance

cases are not counted as failures.

Banks That Subsequently Failed

Banks That Did Not Fail

Agricultural banks are banks where agricultural loans are at least

25% of total loans.

1980 1982 1984 1986 1988 1990 1992 1994

1980 1982 1984 1986 1988 1990 1992 1994

1980 1982 1984 1986 1988 1990 1992 1994

1980 1982 1984 1986 1988 1990 1992 1994

10

20

30

10

15

20

25

3

4

5

*

6

10

14

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

30 History of the EightiesLessons for the Future

Table 1.5

Selected Financial Ratios

A. Failed and Nonfailed Banks 1 Year before Regional Recession

1981 1989 1990

Agricultural Banks Southwest Banks Northeast Banks California Banks

Ratio Failed Nonfailed Failed Nonfailed Failed Nonfailed Failed Nonfailed

Equity/Assets 7.91% 8.30%* 7.00% 7.63%* 6.67% 9.21%* 5.71% 10.47%*

Eq.+Loss Res./Assets 9.11 9.77* 8.64 9.25* 8.34 9.93 7.20 11.46*

Nonprfm Lns/Tot Lns NA NA NA NA 8.60 2.95* 6.23 2.39*

ROA 1.26 1.33 1.22 1.38* -1.68 0.67* -0.63 0.36

ROE 16.90 16.44 18.98 18.99 -23.65 6.73* -7.78 9.88*

Loans/Assets 56.30 48.48* 53.94 47.72* 75.16 68.05* 73.12 69.63

Comm. Mtgs/Assets 2.08 2.19 3.92 3.42* 13.91 9.44* 10.79 11.91

B. Failed and Nonfailed Banks 3 Years before Regional Recession

1979 1987 1988

Agricultural Banks Southwest Banks Northeast Banks California Banks

Ratio Failed Nonfailed Failed Nonfailed Failed Nonfailed Failed Nonfailed

Equity/Assets 7.39% 7.87%* 6.94% 7.45%* 7.96% 8.86%* 6.95% 9.58%

Eq.+Loss Res./Assets 8.85 9.45* 8.45 9.08* 8.53 9.37 8.02 10.52

Nonprfm Lns/Tot Lns NA NA NA NA 1.70 1.14* 4.86 2.28*

ROA 1.15 1.28* 1.00 1.28* 0.62 1.04* 0.08 0.78*

ROE 16.10 16.64 15.55 17.80* 11.66 14.32 2.29 10.85

Loans/Assets 58.40 55.56* 53.42 50.02* 74.31 66.33* 68.72 63.01*

Comm. Mtgs/Assets 2.13 2.42* 3.99 3.71 13.08 8.25* 7.78 8.76

Note: Data are unweighted averages of individual bank ratios. Asset and loan figures are year-end values of the given year,

and equity figures are year-end of the previous year. Excluded were banks chartered within the specified year, banks that

failed before the recession, and banks participating in the Net Worth Certificate Program. Nonperforming loans were not re-

ported before 1982.

*Significant at 95 percent level

33

The comparison in California is between failing and surviving banks with assets below $300 million. All but one of the

states bank failures were in that asset-size group, while the total state data are dominated by Californias four megabanks

(see Chapter 11).

mercial mortgages were higher relative to total assets for failed banks. Banks that would fail

also had lower equity-to-assets ratios than survivors in the year before the recession.

33

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 31

34

The 198090 period was selected in this comparison to compensate roughly for the fact that banks chartered between 1991

and 1994 did not have as much chance to fail during the period through 1994.

Three years before the onset of the regional recessions, banks that would fail likewise had

significantly higher ratios of loans to assets, but these banks equity-to-assets ratiosal-

though somewhat lower than those of banks that would survivewere in the generally

healthy range of nearly 7 percent to nearly 8 percent (table 1.5).

These results are generally consistent with the findings on measures of risk and con-

dition summarized below in the section on off-site surveillance. As noted in that section,

five years before their failure, banks that would subsequently fail differed little from banks

that would survive in terms of equity-to-assets ratios and other measures of current condi-

tion. On the other hand, banks that would fail had higher loans-to-assets ratios than sur-

vivors, and high loans-to-assets ratios were the risk factor with the strongest statistical

relationship to incidence of failure five years later.

Although high loan volumes were a prominent feature of failing banks from 1980 to

1994, they obviously were not an automatic route to failure. Banks earn income by manag-

ing risk, including risk of loan defaults. The averages of individual bank ratios discussed

above obscure the fact that some banks that survived also had high concentrations of assets

in total loans and/or commercial mortgages. Similarly, as noted below in the section on off-

site surveillance, only a fraction of the banks with high loans-to-assets ratios would fail five

years later. The conditions enabling many banks with high-risk financial characteristics to

survive the recessions and avoid failure may include the following, among others: strong

equity and reserve positions to absorb losses, more-favorable risk/return trade-offs, superior

lending and risk-management skills, changes in policies before high risk was translated into

severe losses, improvements in local economic conditions, and timely supervisory actions.

High lending volumes may lead to trouble if a bank achieves them by relaxing credit stan-

dards, entering markets where management lacks expertise, or making large loans to single

borrowers, or if loan growth strains the banks internal control systems or back-office oper-

ations. That such factors were present at many banks that failed from 1980 to 1994 has been

suggested by numerous observers, including those interviewed during the research for this

study.

New and converted banks. Approximately 2,800 new banks were chartered in the pe-

riod covered by this study, 39 percent of them in the Southwest (notably Texas) and Cali-

fornia. Of all the institutions chartered in 198090,

34

16.2 percent failed through 1994,

compared with a 7.6 percent failure rate for banks that were already in existence on De-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

32 History of the EightiesLessons for the Future

Table 1.6

Failure Rates, Newly Chartered and Existing Banks

Banks Chartered, 19801990

Number Failed Percent Failed

Region 19801994 19801994

Southwest 248 33.3

Southeast 26 4.3

Northeast 38 19.3

California 41 13.1

U.S. 420 16.2

Banks Existing on December 31, 1979

Number Failed Percent Failed

Region 19801994 19801994

Southwest 538 21.4

Southeast 77 3.1

Northeast 89 8.5

California 31 12.8

U.S. 1,114 7.6

35

A study of the Texas experience concluded that the relatively high failure rate for newly established Texas banks can be

explained by high-risk financial policies (Jeffery W. Gunther, Financial Strategies and Performance of Newly Estab-

lished Texas Banks, Federal Reserve Bank of Dallas Financial Industry Studies [December 1990]: 13).

36

In the Southwest and Northeast, newly chartered banks failed with greater frequency than preexisting banks, whether

newly chartered includes all banks chartered during the 198090 period or only those that were in existence for five years

or less. In Southern California, however, failure rates for banks in existence for five years or less were lower than those for

preexisting banks, whereas failure rates for all banks chartered in the entire 198090 period were higher.

37

Jennifer L. Eccles and John P. OKeefe, Understanding the Experience of Converted New England Savings Banks, FDIC

Banking Review 8, no. 1 (1995): 118.

cember 31, 1979 (see table 1.6).

35

Although the data are dominated by the Texas experience,

in most areas banks chartered in the 1980s generally had a higher failure rate than banks ex-

isting at the beginning of the 1980s.

36

In the Northeast, mutual savings banks that converted to the stock form of ownership

represented a somewhat comparable phenomenon.

37

Of the mutuals that converted in the

middle and late 1980s after state legislation permitted such action, 21 percent of the insti-

tutions existing at the end of 1989 failed in 199094. This compared with 8 percent of the

Chapter 1 Summary and Implications

History of the EightiesLessons for the Future 33

Table 1.7

Failure Rates of Converted Mutual Savings Banks and Other Banks,

Northeastern States

Commercial

Savings Banks

Cooperative

Banks Stock Mutual Banks* Total

Number Existing 12/31/89 588 149 211 101 1,049

Number of Failures, 199094 65 32 16 5 118

Percent Failed 11 21 8 5 11

Note: Data are for Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, and Vermont.

* Cooperative banks is the term used for state-chartered savings and loan associations in Massachusetts.

mutuals that existed as of the end of 1989 and had not converted, and 11 percent of the re-

gions commercial banks (see table 1.7). New banks and converted mutuals highlighted in

extreme fashion the problems confronting many other banks in the 1980s. These institu-

tions had strong incentives to expand loan portfolios rapidly in order to leverage high ini-