1

www.galitt.com

WHITE PAPER

Request-to-pay:

No longer the missing link

2

About this white paper & acknowledgements

Both retail payment specialists, Galitt and Sopra Banking Software have come

together to bring you this white paper covering the opportunities offered by

Request-to-Pay (RtP), as well as the issues arising from its implementation.

We would like to thank the Sopra Banking Software’s team, Valérie Bellec, Will

Kitson and Hugues Leclère, whose involvement and continuous support have

permitted to produce this white paper.

3

About Galitt

A reference in the domain of payment systems and electronic transactions, Galitt is the

market leader in France in every one of its business sectors, and throughout the world for its

testing tools and its expertise in innovative technology.

Galitt is recognized for offering a wide range of skills and complementary knowledge to assist

its clients throughout the lifecycle of their projects and in every link of the payment value

chain. The company’s size allows it to take on large projects while retaining its ability to be

reactive, its personal touch and the ambition of an organization that is run on a human scale.

Galitt is the reference in the execution of the most advanced payment technologies and the

definition of tomorrow’s technological architecture.

Galitt’s services are based around 3 Business Units:

• Consulting experts aiming to develop targeted proposals: marketing,

innovation, digital transformation, regulation, security and payment

cybersecurity

• Projects & Services experts in development and tests, who benefit from

Galitt expertise in payments, and whose skills cover the whole value chain

• Platforms teams whose engineers and specialized technicians develop

testing software and take part in both the industrialization phase of

testing and the certification of solutions

Galitt is a Sopra Steria Group company. In 2019, Galitt achieved a turnover of €35

million and employed 320 people.

To find out more about Galitt, please visit our website at: www.galitt.com

Contact Galitt

Jean-Michel Mamann

Executive Director

Mobile: +33 6 33 05 23 31

jean-michel.mamann@galitt.com

4

Foreword

In a remarkably short space of time, payment evolution has ushered in an era where convenient,

secure and agile solutions have appeared in each sector, segment and corner, revolutionizing the way

money is exchanged and business is done. Although commonplace, this has never been truer than

with Request-to-Pay (RtP). This “missing link”, through which payees (beneficiaries) can together

trigger and simplify fund transfers, is nothing less than a game changer. Rarely has a standard been

so anticipated.

A few weeks ahead of RtP’s SEPA-wide launch, this joint Galitt-Sopra Banking Software white paper

makes the case for and outlines a promising, steady wave of innovative services, suiting the need of

consumers, SMEs and large organizations alike. This paper explores RtP’s benefits over existing

payee-initiated operations (card, direct debit) and over current e-billing mechanisms: reduced costs

and user friendliness, as well as better tracking and reconciliation information, just to name a few.

On top of how RtP works in mainland Europe, and its market potential in light of preceding overseas

rollouts, this paper also outlines significant business use cases across customer segments: person-to-

person, consumer-to-business and business-to-business. The analysis is supported by original

research on consumer billing transactions’ potential to move to RtP. It clearly shows a practical

interest from all categories of would-be users. From the relatively wealthy to millennials to more

financially challenged populations, there is an unquenched demand for more control and flexibility in

bill payments.

Finally, this paper focuses on how implementation is optimized for Payment Service Providers (PSPs),

among all categories of RtP service providers.

With this program, Sopra Banking Software and Galitt hope to share a new vision of RtP in Euro, from

the curious to the savvy. We hope it makes for interesting reading.

5

Table of contents

1. Recent innovations have paved the way for Request-to-Pay 7

1.1. Ubiquity of digital banking services 7

1.2. Instant Payment’s roll-out 7

1.3. Guidelines for interoperable Electronic Invoice Presentment and Payment (EIPP) 8

1.4. Early RtP-like features in solutions around the world 9

12

2. A highly anticipated SEPA-wide standard 14

3.1. Easing the way to be paid 14

3.2. The EPC scheme’s choices 14

3.3. Enabling a diversity of RtP-based use cases on all significant markets 17

2.3.1. B2C mobility – Pay now 20

2.3.2. B2B – Invoice presentment and payment - Planned pay later 21

2.3.3. C2B POS purchase - Pay now 22

3. A vast market potential across SEPA 24

4.1. RtP perspectives in the European ‘patchwork’ landscape 24

4.2. An unfulfilled need: Toward a more flexible billing 26

4. Key recommendations for implementation in IT systems 31

4.1. The RtP ecosystem and a possible opportunity left to PISPs roles 31

4.2. Adapting the implementation strategy to the specifics of each IT system 32

4.3. Implementation challenges to overcome 32

6

082010 - White paper Galitt – Request-to-Pay

Recent innovations have

paved the way for

Request-to-Pay

1

7

082010 - White paper Galitt – Request-to-Pay

1. Recent innovations have paved the way for Request-to-Pay

The highly anticipated Request-to-Pay service in Europe has not come from nowhere. Rather, the

standardization of this payee-triggered payment facility coincides with the recent availability of many

of its key enablers.

1.1. Ubiquity of digital banking services

As the digital world has gained momentum and become part of our everyday lives, there has been a

rapidly growing demand for flexible, richer banking services. People of all ages are increasingly

connecting 24/7 to their financial data, with millennials the most engaged generation. Right on their

heels, Generation Z (typically defined as those born between 1997 and 2012) is expecting and

demanding new services to satisfy its growing requirements in terms of customer experience and

technology, especially mobile technology.

In recent years, we have seen non-traditional players entering the banking market. These new

entrants are better placed to satisfy the digital needs of consumers, while traditional banks are faced

with significant challenges, such as eroding revenues and legacy cost bases. These mostly result from

new entrants focusing on user experience, with a young brand image, light structures and the aim to

create innovative and exciting services.

Neobanks and digital-savvy financial services firms - such as N26, Revolut and Monzo - have been a

catalyst in the industry, inspiring traditional banks to evolve both the content and the “look and feel”

of their online (web and mobile) banking services.

Furthermore, recent regulations - such as PSD2’s ongoing implementation - which aim to protect

customers and to formalize the use of new technologies, are yet another driver for Financial Services

(FS) firms to adapt their digital offerings. For traditional and non-traditional banks alike, the must-

have strategy is to compete in building a digital bank.

This has led to rapid advancements in recent years from traditional and emerging FS firms alike. Credit

transfer, in particular, has become increasingly convenient, fast and cost efficient, thanks to

technological advances in digitization and data processing. Today, it is nearly a daily routine for

anyone connected through mobile or e-banking - a huge leap from the not-so-old branch-and-paper-

based approach. This is reflected in cash and cheque’s significant decline in recent years.

Now a must-have dimension of any financial institution’s offering, digital services provide customers

with tools to manage all aspects of their payment needs: communicate with their counterparts

(payees, payers), track flow of money, manage their bill payments and pay – all in an instant.

Considering all these features, when adopted by all players along the payments value-chain, Request-

to-Pay has the ability to be a real game changer.

1.2. Instant Payment’s roll-out

Following several national initiatives, SEPA Instant Credit Transfer (SCT Inst) was launched on

November 21, 2017 as an optional European Payment Council (EPC) payment scheme. As of March

this year, 53 percent of European payment-licensed financial institutions - 2,158 payment service

providers (PSPs) - were operating SCT Inst payments SEPA wide1. In October 2019, there were

1

Source: EPC Newsletter, 31 March, 2020

8

082010 - White paper Galitt – Request-to-Pay

already over 3 million payments per week processed in SCT Inst, with 99 percent of transactions

settled in less than 3 seconds.

Instant Payments in Europe has been building on the success of earlier initiatives – from the UK’s

Faster Payment back in 2008 to Spain’s Bizum in 2016, as well as Sweden’s Swish (2012) and Italy’s

Jiffy (2014), just to name a few.

In turn, Instant Payment's’ steady roll out makes it the second driving force for the upcoming Request-

to-Pay (RtP) initiative. Online banking/digitization of payments means that retail payments can be

made from anywhere. Instant Payment ushers in another major quantum leap by eliminating time

delays when making payments. On top of real time, SCT Inst is available round the clock, throughout

the year. It is available day and night with immediate results.

Furthermore, it provides instantaneous finality by design to each unitary payment. This means a

dedicated, underlying interbank system (e.g. TIPS) settles each operation in real time, unlike today’s

mass retail payments, where this occurs later in batches. In practice, it is tantamount to payment

guarantee. Beforehand, this was a privilege restricted to a very small number of high-worth

transactions, directly settled in central bank systems – the so-called TARGET2 payments.

To this end, a pan-European infrastructure has been successfully running since the end of 2018.

Operated by the European Central Bank (ECB), the TARGET Instant Payment Settlement (TIPS)

system provides the final and irrevocable settlement of Instant Payments – in the Euro currency, for

the time being. This also confers SEPA-wide reachability to Instant Payment-enabled PSPs.

Finally, it is also paramount from a legal perspective that Instant Payments can rely on an EU-

governed infrastructure (TIPS), just like its scheme – SCT Inst. This already makes it the target

payment instrument of the future. In the long run, it should become the new norm for credit transfers,

of course, but also for other retail payment operations – as hinted at by the European Payment

Initiative (EPI).

1.3. Guidelines for interoperable Electronic Invoice Presentment and Payment

(EIPP)

Any corporate accountant’s dream is to have outgoing invoices easily matched with customers’

incoming payments – and vice-versa. Dematerializing, exchanging and tracking invoices is the first

step toward achieving this. Whether they are blockchain-based or enabled by an older technology,

the egg-and-chicken dilemma remains the same, whatever the solution: Which e-invoicing provider

has enough coverage to convince an ample number of customers and suppliers to sign up to its

offering?

This “network-effect” roadblock was the cornerstone of an EU Commission initiative when, in early

2009, it launched the European E-Invoicing (EEI) expert group. The EEI taskforce brought together a

team of suppliers and corporate user representatives. Within a year, it delivered a report focusing on

interoperability hurdles and recommendations. This would have simply been yet another smart report

with little practical application were it not for the Euro Retail Payments Board’s (ERPB) later decision

– made after SEPA (SCTs, SDDs) had gone mass market – to accelerate further innovation and

standardization around core payment.

With the ambition still firmly in its sights, the SEPA decision-making body put truly interoperable EIPP

on its roadmap. In November of last year, an EPC-led stakeholder group delivered practical guidelines,

building a convincing base for what had in parallel grown as one of RtP’s emerging use cases.

9

082010 - White paper Galitt – Request-to-Pay

1.4. Early RtP-like features in solutions around the world

Designed to provide businesses and consumers with greater flexibility when making payments, these

RtP features allow the payee to add relevant data in order to process receivables and, in some cases,

receive confirmation that a payment order has been issued. Some of the standard use cases of RtP

include P2P, B2B and B2C payments (e-billing/invoicing, e-commerce payments and point-of-sale

payments).

In most cases, the payment request is generally a hyperlink sent by a payee to a payer. It redirects the

payer to a secure checkout, where the requested payment occurs either through prefunding, debiting

a bank account or a card payment. Request links may be sent via e-mail, SMS, QR code or chat

applications, such as WhatsApp or Messenger.

Request-To-Pay initiatives around the world by use-cases

Designed to provide businesses and consumers with greater flexibility when making payments, these

RtP features allow the payee to add relevant data in order to process receivables and, in some cases,

receive confirmation that a payment order has been issued. Some of the standard use cases of RtP

include P2P, B2B and B2C payments (e-billing/invoicing, e-commerce payments and point-of-sale

payments).

In most cases, the payment request is generally a hyperlink sent by a payee to a payer. It redirects the

payer to a secure checkout, where the requested payment occurs either through prefunding, debiting

a bank account or a card payment. Request links may be sent via e-mail, SMS, QR code or chat

applications, such as WhatsApp or Messenger.

Focus on European RTP-like operational features

10

082010 - White paper Galitt – Request-to-Pay

A number of Request-to-Pay initiatives have already been implemented in several countries – all 4-

corner-model based:

• In Australia, BPAY is the most widely used bill payment service. It enables payers to transfer

funds electronically from their bank accounts to billers. BPAY can be used with over 45,000

businesses in Australia, and each month it processes 30 million individual payments. The

number of BPAY payments increased by an average of 3.3 percent between 2012 and 2018

• In Nigeria, Remita, adopted by the Central Bank of Nigeria, enables all kinds of billers to

receive C2B payments: educational institutions, insurance companies, e-commerce shops,

utility companies, clubs and associations, religious organizations and governments. Remita is

offered by all commercial banks and more than 500 microfinance banks in Nigeria, as well as

several public and private organizations. It processes over 700 billion Nigerian naira every

month

•

In the Netherlands, all major Dutch banks own and participate in Currence, the multi-

instrument scheme that operates iDEAL, the most-used local online payment method with a

share of online transactions close to 55 percent. iDEAL has recently started offering a

Request-to-Pay feature, which is becoming more and more popular. By early 2019, no less

than 17.5 percent of all iDEAL payments were accounted for by C2C-payments (Consumer-

to-Consumer), mainly as a result of Requests-to-Pay with Tikkie and other mobile payment

apps from Dutch banks.

In addition to these mature RtP solutions, a series of open-loop initiatives are also emerging in

Europe:

• In the UK, Pay.UK is rolling out RtP after a successful pilot and is scheduled to go live during

2020 (Visa has supported the pilot by facilitating the first message sent and received). (See

insert below)

11

082010 - White paper Galitt – Request-to-Pay

• In March 2020, Hungarian banks launched an Instant Payment System (AFR in Hungarian),

based on the EPC’s Instant Payment scheme (SCT Inst). This new core retail system, allowing

instant credit transfer services, is able to manage Request-to-Pay messages

• At pan-European level, the EPC has committed to launching a Request-to-Pay scheme in

euros toward the end of 2020, described in detail in Chapter 2

Request-to-Pay adoption is likely to increase in the coming years in Europe, especially in markets with

low-card usage, such as the Netherlands and Germany, where credit card penetration is lower than

50 percent of all payment instruments.

“The British Request-to-Pay”

AccessPay is a payment and cash management software provider, offering a range of products such

as Direct Debit, SEPA, Faster Payments, SWIFT and Multi-Bank Cash Management. Danny Doyle is

head of product management at AccessPay and a Member of Pay.UK’s RtP working group.

Could you give us an update on RtP in the UK?

D. Doyle: Request-to-Pay is a flexible way for payments to be settled between people,

organizations and businesses. In the UK, Pay.UK set the RtP standards. It is agnostic and

supports messages between the payer and the payee, who may have different service providers

(third-party operators). The repositories that route and store messages could be operated by

banks and non-banks, such as PISP-licensed operators, technology vendors and utilities. The

flexibility to integrate an RtP service developed by multiple and diverse parties led businesses

into uncertainty, as RtP involves many stakeholders. Conversely, EPC’s RtP is bank-driven and

largely embedded in SEPA banks’ customer interface, i.e. mobile and web banking apps.

Interview with Danny Doyle of AccessPay:

12

082010 - White paper Galitt – Request-to-Pay

What are the benefits/advantages you see in the upcoming RtP?

D. Doyle: In addition to benefits such as cost reductions from migration to electronic billing from

paper, reduced time and effort in chasing payments, and increased reconciliation, RtP provides

multiple benefits for public organisms as well as not-for-profit organizations, with improved

communication, reduced admin and streamlined processes. In this time of economic crisis, due

to Covid-19, RtP may provide answers. Indeed, there is a willingness and a need to make

payment terms more flexible, especially for those who are most vulnerable. For local organisms,

such as housing associations, RtP appears less costly by reducing the risk of failed payments and

the time taken chasing them, assuming that consumers co-operate fully. For charities, it can

increase donor retention and provides a flexibility to donors in their payments by offering them

the ability to avoid cancelled standing orders, while maintaining the ability to pay another at a

later date.

Is AccessPay considering positioning on a Request-to-Pay offer?

D. Doyle: AccessPay has been working on an RtP solution compatible with Pay.UK and SEPA

standards, as the majority of their customers are abroad. AccessPay already completed Request-

to-Pay pilot trials and is currently working on evaluating the offering from a business model

perspective for launching a live product for their customers. B2C involving an application is seen

as a growth area.

13

082010 - White paper Galitt – Request-to-Pay

A highly anticipated

SEPA-wide standard

2

14

082010 - White paper Galitt – Request-to-Pay

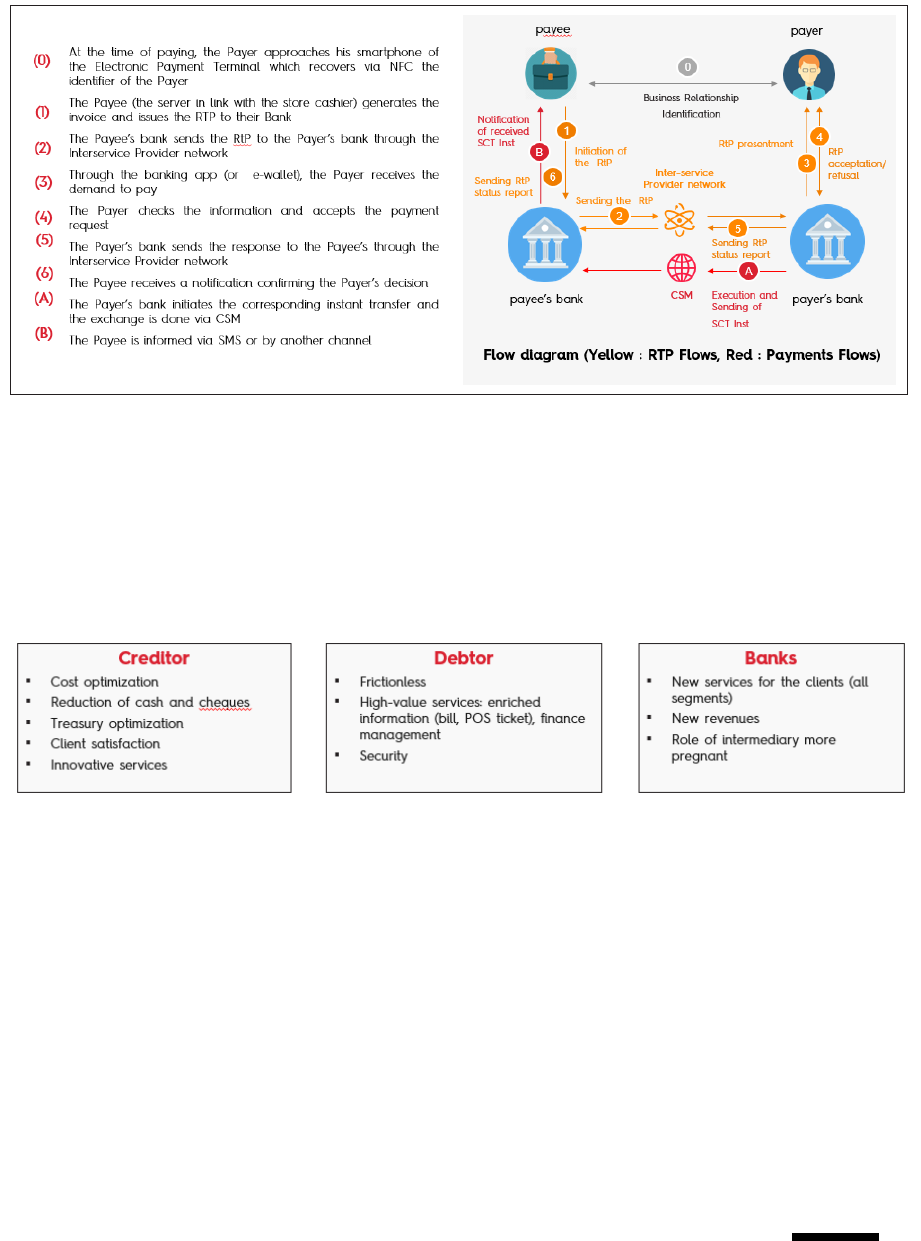

2. A highly anticipated SEPA-wide standard

Since the RtP feature has already been widely documented, in particular around the use of

standardized ISO messages, this white paper focuses on the EPC’s outcome and its promises for

SEPA.

3.1. Easing the way to be paid

In a nutshell, Request-to-Pay is a mechanism allowing a payee (beneficiary or creditor) to send a

message to a payer (debtor) requesting a payment. Through a RtP flow, a payer receives a request

with information provided by the payee, such as execution date, purchase or invoice details or

purpose, and payment amount.

When a payee adds large payment details, such as a full/pro-forma invoice, the payer may access it as

an attachment/download link and then make an informed decision.

If foreseen by the payee, the payer may be offered a choice of payment features, such as due date

flexibility, partial payment and fixed installments.

In all cases, accepting the request will automatically trigger the credit transfer.

3.2. The EPC scheme’s choices

What?

Following a mandate from the ERPB, design of the Request-to-Pay scheme in euros has been

completed by the EPC. Representing all European banks, the EPC is already the designer and scheme

owner of the SEPA payment schemes for credit transfer (SCT), Instant Payment (SCT Inst) and direct

debit (SDD).

This SEPA RtP corresponds with the actions that take place between:

• the commercial transaction (sale) with customer choice of RtP for checkout

and

• the payment execution (by the payer’s financial institution) through a credit transfer

(ordinary or immediate)

It is, therefore, not a payment instrument, but rather a solution to trigger a payment. The EPC defines

it as the set of operating rules and technical elements (including messages) that allow a payee to claim

an amount of money from a payer for a specific transaction.

How?

The RtP scheme will operate around the clock and throughout the year (365/7/24), with instant

routing of all RtPs.

The process occurs in two stages:

1. Presentation: the payer instantly receives the RtP generated and filled in by the payee

(beneficiary)

2. Acceptation: the payer accepts the RtP, followed either by an immediate or by a future payment,

or refuses the RtP

Depending on the payee’s choice, the payer has one of these two options when accepting:

15

082010 - White paper Galitt – Request-to-Pay

• Accept Now: the RtP must be accepted or refused upon reception (very short expiry time)

• Accept Later: the payer may decide within a maximum time range set by the payee (no more

than three months)

The Request-to-Pay message also contains information to specify the resulting credit transfer

operation:

• On payment initiation timing:

Pay Now: credit transfer is initiated immediately after RtP acceptation

Pay Later: credit transfer occurs later – either fixed by the payee or chosen by the payer

within a payee-defined time limit

• On the credit transfer’s speed:

Instant: the resulting payment will be processed by an Instant Payment credit transfer

(e.g. SCT Inst)

Ordinary: the resulting payment occurs by means of an ordinary credit transfer (e.g. core

SCT, MT 103, local transfer in Euro) to be executed within one working day (as PSD2-

required)

To these ends, a timestamp is part of each RtP.

Subsequent, optional features are available to the payee to deal with errors or other issues, such as:

• RtP Cancellation (RfC), available until the RtP’s expiry date (therefore excluded in the “Pay

Now” option)

• RtP Status Update, to investigate a previously sent RtP or RfC

Who?

This scheme introduces a new role, the RtP Service Provider (RtP-SP): one for payee and another for

the payer. To manage RtP flows, these players are interconnected (the so-called “inter RtP-SP”

domain). The RtP provider role is distinct from the payment-licensed financial institution - the PSD2

“Payment Service Provider” (PSP). As the payment account servicing institution, the latter is in charge

of processing the resulting credit transfer and moving the funds.

By contrast, the RtP-SP is not responsible for moving funds and currently does not require official

approval by, or declaration to, a financial regulator or National Competent Authority (NCA).

It may or may not be one of the PSP financial institutions – although it is very likely that payer PSPs

across SEPA will endeavor to be able to process incoming RtPs and present them to their customers.

Other players have a keen interest in the RtP-SP role: e-commerce technical providers, e-invoicing

solution suppliers and mobile-SCT enablers (MSCT / mobile-SCT providers).

Furthermore, Payment Initiation PSP (PISPs) may come into the picture, whether or not they hold the

role of RtP-SP for either or both the payee and the payer.

16

082010 - White paper Galitt – Request-to-Pay

“Combining both the roles of PISP and merchant RtP provider in the subscription

economy”

SlimPay is a French payments institution, accredited since 2010 and European leader in recurrent

payments in the subscription economy. SlimPay offers its retail customers cash collection and

account management services for SEPA payment instruments (transfers and direct debits) and bank

cards. Its key objective is to popularize recurring payments as part of digital experiences.

What do you think about the future Request-to-Pay standard?

SlimPay: We are interested in “pull” payment solutions, where the payee presents the payer

with the transaction as part of a dynamic customer experience integrating Instant Payment.

We have observed that the subscription payment is a well-developed concept; for example,

when purchasing digital contents in the automotive industry (long-term leases, servicing and

maintenance) and even for NGOs, which is highly promising for our business.

What customer gains do you think RtP can bring?

SlimPay: We think that it’s an opportunity for retailers, who will offer enhanced subscription

experiences, based on full transparency with regard to customer commitments. Retailers will

foster a trusting relationship by obtaining the payer’s consent for a series of payment

transactions, which is enabled by RtP. Moreover, it’s an opportunity to gain customer loyalty.

RtP will have the advantage of facilitating exchanges on payment terms between the payee and

the payer. This will mean the payee can change payment dates, defer payment or make several

installments.

Conversely, existing payment instruments have significant shortcomings from the retailer’s

point of view: uncertainty over funds for the SDDs, transaction costs and complexities in

implementing online card payments with 3D-Secure v2.

What are RtP’s aims and what are the next steps?

SlimPay: We are positioning ourselves as a payee RtP service provider, i.e. for the retailer. We

will manage RtP for our retail customers and interact with the payer’s RtP service provider, i.e.

the customer’s.

In addition, we will initiate transfer transactions using banks’ PSD2 APIs, but at this stage we

know that some points need to be clarified. For example, we must interact with the payer’s RtP

service provider as a PISP, and we are wondering what data will enable us to identify this

provider. We must also think about the customer experience and work with RtP providers on

these aspects.

Therefore, we think that RtP solutions have a great deal of potential in the future and that they

complement existing solutions and usages.

Interview with Jérôme Traisnel and Julien Paris, CEO and Product Manager at SlimPay respectively

17

082010 - White paper Galitt – Request-to-Pay

When?

Business legislations were published on June 2, 2020 under the form of a draft-dedicated RtP Scheme

Rulebook for a Europe-wide public consultation throughout the summer of 2020. Separated from the

SCT and SDD rulebooks, although compliant with them as well as with non-SEPA credit transfer

schemes in Europe, the scheme rules will be amended and approved by the EPC for publication at the

end of November 2020. No one-year implementation period will be required. On the contrary,

commercial offers from RtP Service Providers (RtP-SPs) will be immediately possible.

This intended SEPA go-live will provide the basic components of an RtP service, as outlined in a

preliminary EPC framing study endorsed in November 2019 (RtP-specifications for a standardization

framework). Additional components envisioned in this Framework (installment payment, payment

guaranty, etc.) will be included in a secondary version of the RtP Rulebook announced end of 2021.

3.3. Enabling a diversity of RtP-based use cases on all significant markets

Beyond its content, the EPC scheme provides a base for a diversity of added-value services.

Combining the above-two criteria (Accept Now / Accept Later and Pay Now / Pay Later) allows for the

coverage of all significant payee use cases, which belong to one of three segments (according to the

EPC):

• P2P (peer-to-peer): between two physical persons (including sales between two individuals)

• C2B (consumer-to-business): merchant transactions, usually a physical person paying a

commercial entity, either face to face (POS) or remotely (m- and e-commerce; utility billers)

• B2B (business-to-business): EIPP, where an invoice attached to the RtP allows suppliers to

track and reconcile incoming payments

When specifying the resulting transfer (instant or ordinary), this leads to more specific use cases:

• On C2B segment:

Instant payment (SCT Inst) to provide immediate certainty to the merchant

Payment guarantee (outside the EPC scheme)

Multiple payments (installments, subscription)

Pre-authorization (i.e. for traditional T&E use cases: hotels, car rentals, fuel dispensers,

etc.)

• On P2P segment:

Instant or future payment

Embedded or not in P2P messaging / chat services

• For EIPP / e-invoicing:

For C2B (utility billers): e-invoicing with instant or deferred payment, and with or without

payment guarantee

For B2B: on top of bill reconciliation, e-invoicing may offer options to the payer such as

partial payment, forwarding the RtP to another party for financing purposes and bundling

multiple RtPs into one payment. The B2B payee may also receive a guarantee of payment

18

082010 - White paper Galitt – Request-to-Pay

User gains from the RtP innovation

19

082010 - White paper Galitt – Request-to-Pay

“Coupled with Instant Payment, RtP opens up promising business transformation

opportunities”

Isabelle Charlier is responsible for banking relations and transformation projects linked to means of

payment within the Treasury Department of Allianz France’s Investment Division. Allianz France is a

subsidiary of Allianz SE, whose headquarters are in Munich. Under her responsibility, Benjamin Hort

is a Project Manager in charge of innovation and is currently leading the Instant Payment project.

What do you think about the future Request-to-Pay standard?

Allianz France: We are convinced that it will be a must have for cash collection, and that it will

drive the use of real-time transfers. We already have a pilot project on real-time transfers in

France, and the Group is keen to see what the results are.

What customer gains do you think it can bring?

We can see various promising applications that combine RtP and real-time upstream. For

example, improving customer retention by offering an immediate debit to pay the premium

amount before contract termination date. In addition to reducing contracting costs, the transfer

helps to avoid constraints when it comes to managing payment personal data used for card

payments, subject to PCI-DSS security requirements.

Another example is real-time prolongation of an existing insurance policy. This means we can

extend guarantees to a new mode of transport (electric scooters, mopeds, high-end vehicles,

etc.) or new activities, such as extreme sports. In order to be immediately effective, the

amendment signature will be followed by the premium payment in real time. This will improve

customer dialogue and reduce the number of disputes in case of claims.

Can we imagine scenarios where RtP triggers an ordinary transfer?

Yes, and in this instance, we will have another string to our bow to speed up the process of

phasing out the use of cheques by customers who are hesitant to switch to automatic direct

debits. This will provide us with a better alternative to interbank payment orders (the single-use

paper version of the direct debit). For some time, we have seen that this process has levelled out

and cheques are still subject to a great deal of fraud. Furthermore, RtP will enable us to replace a

fraction of ordinary transfers received, for which account lettering is tedious.

Interview with Isabelle Charlier and Benjamin Hort of Allianz

20

082010 - White paper Galitt – Request-to-Pay

As seen above, the EPC RtP scheme caters for a variety of implementations, in particular through its

multitude of options, and the possible declination to 2-, 3- and 4-party models. To illustrate, we have

highlighted below three use cases that have the potential to become mainstream, focusing on the

benefits of each one. Note that all rely on instant payment to benefit from the finality of payment.

To simplify these use cases (all in a 4-party model), each bank (for payers and payees) combines the

role of RtP Service Provider and of Payment Service Provider (PSD2 licensed financial institution) for

their respective customer (payer / payee). Of course, separate stakeholders may hold each of these

roles.

2.3.1. B2C mobility – Pay now

The first promising use case is a B2C payment in a mobility context. To ensure finality of payment, it

is implemented with the “Pay Now” feature.

Let’s say that a plumber performs a service at a private individual’s home and gets paid on the spot,

once the service has been concluded.

How RTP operates in B2C

21

082010 - White paper Galitt – Request-to-Pay

2.3.2. B2B – Invoice presentment and payment - Planned pay later

For B2B payments, RtP offers huge potential for truly interoperable e-invoicing.

In this example, we will look at an automotive supplier wishing to improve its productivity for invoice

collection.

How RTP operates in B2B

In this use case, the payee’s e-invoicing solution could offer the option to settle several invoices

through one single payment; for instance, at the end of the month. When one SCT settles several RtPs

(and their attached invoices), EPC’s Extended Remittance Information (ERI) SEPA option could be an

efficient function to optimize reconciliations and to reduce the number of payments.

22

082010 - White paper Galitt – Request-to-Pay

2.3.3. C2B POS purchase - Pay now

Our last significant use case applies RtP to in-store payment in a frictionless way, allowing the easy,

paperless reconciliation of sales with payments.

How RTP operates in C2B

Using end-to-end references, it is easy for the payee (merchant) to reconcile sales and payments.

Importantly, the whole process must be at least as quick as a card payment to ensure adoption by all

stakeholders. It may, however, fully coexist with card acceptance in order to reduce the use of cheques

and cash.

23

082010 - White paper Galitt – Request-to-Pay

A vast market potential

across SEPA

3

24

3. A vast market potential across SEPA

First off, we have estimated future European RtP usage by projecting the current proportion of RtP

transactions in relation to the number of credit transfers in Australia, a geography where RtP has

already been rolled out and well documented. The aim is to approximate the volume of Europe’s

cashless transactions that could potentially switch to Request-to-Pay based solutions for B2B, B2C

and B2G use cases.

In parallel, for a deeper understanding of market needs, we have focused on B2C billers’ use cases,

where we see the first and most likely RtP quick win. To this end, a quantitative consumer survey

highlights the RtP benefits for payers, billers and their respective financial institutions.

4.1. RtP perspectives in the European ‘patchwork’ landscape

Each country in Europe has its own cashless payment culture: mostly either card-predominant (in pink

below) or credit-transfer dominant (in blue).

Number of retail payments transactions in Europe in 2018

(Total number of payments) Source: ECB (European Central Bank)

Overall, cards remain the most prolific payment method in Europe, accounting for 54 percent of all

payments. Card payments are especially used in daily purchases, such as food shopping, utilities,

entertainment, etc. Credit transfers, the second most-used payment method, account for 22 percent,

while direct debits, the third most-common method, account for 18 percent. (Cash payments have

not been

included in this analysis).

25

In a first approximation, we have used Australia’s figures for BPAY, the local interbank system for C2B

and B2B e-invoice settlement (EIPP), public sector included. It has now been widely used there for two

years. We are, therefore, projecting the Australian adoption rate onto European credit transfer

volumes two years after the SEPA RtP rollout, which is due to take place in full in 2022.

This gives us a rough market estimate for Request-to-Pay of 4.9 billion transactions per annum in 2025

– linked to fully Europe-wide interoperable EIPP systems (to compare with the Australian reference).

This would exceed the current level of cheques, which is already low.

E-invoicing growth and interoperability are more likely to materialize since the EU Directive

2014/55/EC makes it mandatory by the end of 2020 to include an e-invoicing feature in every B2G

procurement relationship with regional or local public authorities. The aim is to make e-invoicing the

primary invoicing system in Europe. According to a Billentis survey

2

, e-invoicing has already

reached 5 billion consumer customers and 8 billion business and government customers.*

2

Koch, B., E-Invoicing / E-Billing: Billentis January 2019

The Public Finances Directorate General (DGFiP) collects individual taxes, business taxes and the

central government’s non-tax revenue from regulatory and statutory fines, court-imposed fines,

miscellaneous income, etc. The treasury’s DGFiP is therefore acting as their (only) cash

management banker, with several offers for their receivables and payables: cheques (80M/year),

cards, transfers, and direct debits. In that field, DGFIP is in charge of the innovation and payment

projects

Galitt: Could you tell us about the need for RtP within the DGFiP?

A.MANOUVRIER: The DGFiP is very involved in the dematerialization of payments for the

impots.gouv.fr website and for public entities, particularly on the subject of Instant Payment

and, more recently, that of Request Payment. The DGFiP intends to be a major player involved in

the development of RtP by becoming itself an RtP provider, while offering an RtP solution

coupled with Instant Payment. The DGFiP is considering the implementation of an application

offering an RtP solution while integrating all types of invoices for public entities. There are

several potential use cases already identified, such as the collection of the state's non-tax

revenue (registration or visa fees, for example); the collection of fines, sanctions and

miscellaneous penalties; the collection of local authority revenues (water, electricity, gas,

canteen, etc.); or management of payment schedules granted for the above-mentioned receipts

and/or tax revenues. The main target of RtP should be down payments made by cheques or

credit cards. In fact, RtP is not intended to replace all existing electronic payments, such as direct

debits, which have been working very well in income taxes.

Interview with Mr. Alexis MANOUVRIER - head of division “treasury system, banking

management” at DGFiP – 16 september, 2020

26

4.2. An unfulfilled need: Toward a more flexible billing

From a biller point of view, direct debit is the most convenient cash-in instrument in terms of payment

automation. In comparison, credit transfers may only be automated on the payer’s side.

When billers roll out their own e-invoicing solutions, it must - until now - be adopted by a large

majority of customers, so that back-office cost savings can offset investment and communication /

education costs.

Otherwise, billers may reduce a fraction of time spent on reconciliation, but only after having correctly

identified the first cash-in for each customer. This excludes all one-shot use cases, especially when

the payer is different from the customer (third-party payer). Otherwise, as estimated by Billentis,

direct staff costs of preparing and sending out paper invoices are believed to be between €2.50 and

€10 per invoice. Receiving and settling paper invoices would be even more costly, at around €5 to €15

per invoice, since the reconciliation needs to be done by hand.

Furthermore, billers lack vision on missed payments, especially on people who would like to buy but

do not have the resources to do so. Request-to-Pay can reduce such payer avoidance due to a lack of

funds. In addition, it improves creditors’ cash-flow, when customers may opt for splitting a due

payment, instead of rejecting it in whole.

Both parties stand to win with RtP:

• Billers will have a new payment feature for those customers who want to opt-in for / decide on

each single due payment

• Consumers will better apprehend and plan their payables while retaining more control of

them, such as choosing how and / or when they settle it

Galitt: What are the benefits you see in the upcoming RtP (coupled with Instant Payment)?

A. MANOUVRIER: The first benefit is its instant nature, since payments would be delivered with

Instant Payment. The second benefit is the cost reduction. In fact, RtP would use Instant

Payment, which is charged at a lower rate compared to other payment methods, such as

cheques or credit cards. The last benefit is a better accounting management on processing and

reconciliation. Indeed, RtP reduces manual inputs and ensures delivery of payment to the right

place.

Galitt: What stage are you at with the development of an RtP solution?

A. MANOUVRIER: The DGFiP has already been working on RtP use cases and thus completed

the first phase of reflection and requirements analysis. The second phase, which consists of

developing an RtP solution, would start in 2021, at the earliest. A service provider would be

chosen by the DGFiP and the Banque de France would be in charge of collecting the flows. The

final phase, which includes the tests, is expected to take place at the end of 2022 and will

certainly be achieved at the beginning of 2023.

27

“An easy, cost-effective way to increase our range of digital cash-in payment

methods”

ACOSS is the French Social Security scheme’s entity in charge of all receivables, such as

family benefits, sick leaves, pensions and professional injuries schemes. Tasked with

ACOSS’s Local Cash Management and Banking Relations, François Bechu is driving the

strategy of payment projects.

What user benefits / advantages do you see in the upcoming RtP?

F. BECHU: For us, RtP is an opportunity to extend our paperless receivables offer to employers,

small and large, on top of direct debit, card payment and so-called (French authorities-specific,

SDD-based) “remote e-payment” (télérèglement). From our viewpoint, SEPA Direct Debit’s

(SDD) mechanism is very handy but is constrained by the legal D+1 execution time. Moreover, it

has an eight-week unconditional dispute risk. Of course, this is very low for us, but non-existent

for credit transfer. Compulsory for some categories of employers, credit transfer guarantees

settlement on the planned D-day (two slots per month). Lastly, RtP certainly will contribute to

the erosion of cheque usage.

What would be the gains for ACOSS as an organization?

F. BECHU: RtP could allow us to initiate payment flows that, until today, do not originate from

our IT back-ends, but from ordering parties’ financial institutions. We should, therefore, improve

our receivables forecast and planning. We would be able to determine the key parameters of

future incoming credit transfers: initiation date, pre-filled reference data and status inquiries on

outstanding RtPs. In particular, as well as an instant payment, we could optimize our liquidity

management between paid-in and paid-out transfers. This would lead to an optimized cash flow

management and, ideally, to lower liquidity supply costs.

What about managing payment instruments?

F. BECHU: We expect a more attractive pricing for transactions. Thanks to credit transfer’s

current business model – as well as the likely increased competition in the RtP service provider

domain -- we may even see some aggressive offers. Direct debit costs little nowadays, but card

payments, which stand for 1.5 percent of our transactions and 0.1 percent of amounts, account

for 60 percent of our payment charges. We have been offering this payment method to

accelerate conversion to paperless payments, especially for self-employed people. The average

value is €600, rising to €30,000 per single payment. However, our card acquirers do not offer us

any discount for such high-value payments. RtP should, therefore, incur a typical credit transfer

pricing, which is not amount-dependent and hence much lower.

Interview with François Bechu of ACOSS

28

RtP: A popular feature even for higher-income consumers

Consumers using automated payment methods, such as direct debit, generally belong to higher- or

medium-income categories, who value the ease of interference-free payment processing. However,

people from lower-income categories tend to rely more on cash and cheques, which offer a reliable

yet paper-based way to monitor and manage their expenses – planned or otherwise.

Current economic uncertainty is poised to become an issue for a significant number of Europeans,

affecting, in particular, an increased share of short-term contracts and self-employed people.

To shine some light on this subject, Galitt conducted a quantitative research study in order to

understand people’s attitudes toward RtP as a new way to settle invoices. Four-hundred-and-fifty

consumers, representative of French society in terms of age, gender, socio-professional category and

national geography, answered an online questionnaire.

Findings

It emerged that 86 percent of the respondents have experienced difficulties paying their bills in the

last 12 months. More importantly, among those in financial difficulty, 77 percent have already

abandoned a purchase because of their financial situation. It is in this context that 71 percent of the

study’s participants said they were interested in RtP (25 percent said they were “very interested”),

especially concerning RtP’s function of delaying the full payment of an invoice or settling the invoice

for a partial amount and splitting the remaining amount in installments.

Finally, regarding the use of RtP, 70 percent of respondents said they would prefer to use email,

compared to WhatsApp (26 percent), a mobile app (26 percent) and Facebook Messenger (20 percent)

due to security concerns.

Do you already foresee an RtP-enabled project?

F. BECHU: RtP should support ACOSS’s ambition to embed payment in compulsory social

welfare reporting. We wish to offer a fluid, end-to-end journey to employers when they report

staff activity. We currently operate our own cash-in solutions for direct debit, remote e-payment

(“télérèglement”) and our dedicated offers. We also operate card acceptance under a white-label

model. Our ambition is to include the payment step in staff activity reporting, which we could

summarize as ”declare and pay”. RtP would provide this link for employers who rely on credit

transfer only, since it would usher along the payment order.

Of course, payer friction will have to be reduced throughout the payment journey. Notable

points of attention, among others, will be entering and checking the payer’s IBAN account

identifier, as well as authenticating the payer customer.

29

30

Key recommendations for

implementation

on IT systems

4

31

082010 - White paper Galitt – Request-to-Pay

4. Key recommendations for implementation in IT systems

The EPC’s Request-to-Pay scheme, integrated with SEPA’s payment schemes, has certain similarities

to existing bank-supported payment collection methods, including direct debit and capabilities

provided by proprietary e-invoicing and payment platforms. Indeed, ensuring the right to adherence

to all categories of trusted solution providers helps the reachability and deployment of RtP.

Nevertheless, the diversity of customer use cases, sometimes complex, may have to overcome

several obstacles in order to achieve wide adoption, especially when we consider, in detail, its

execution in an IT system and an already existing process.

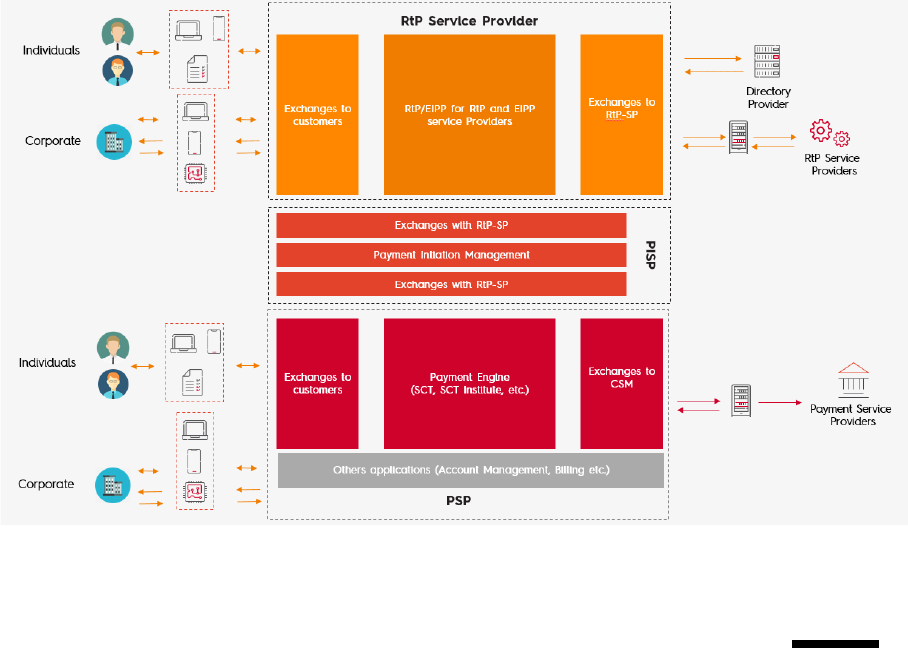

4.1. The RtP ecosystem and a possible opportunity left to PISPs roles

As mentioned in part 2.2 of this white paper, multiple types of organizations can have roles in the RtP

ecosystem. RtP is not a payment service so there is no reason why other functions such as PSPs

couldn’t operate as part of an RtP framework. In fact, the functions that need to be performed as part

of the RtP solution can be done so by financial institutions (payment and credit institutions) as well as

payment processor and technical acceptance processors (PATs), CSMs (clearers) and non-financial

companies.

The representation below shows the different functions for each dedicated actor – who is only

responsible for tasks concerning RtP, as well as exchange channels with clients and other RtP SP –

and PISP for payment initiation.

Distribution of functions for each dedicated actor RTP-SP, PISP, PSP

(high-level vision)

32

082010 - White paper Galitt – Request-to-Pay

However, PISPs could seize this opportunity and play a major role in bridging the gap between banks

and RtP service providers.

4.2. Adapting the implementation strategy to the specifics of each IT

system

The technical implementation of this new solution should be framed in its utility for commercial

purposes in order to rationalize costs and limit the risks on the existing infrastructure for each actor

involved in the process. Although the deployment of Request-to-Pay can be considered overall as an

end-to-end solution, it is necessary to plan for its implementation bearing in mind the following items:

• Prioritize organized work, depending on the most-valued use cases for a fast return on

investment

• The need to offer real-time, widely available services

• Level of service on which to position oneself, and the scope of IT systems impacted by these

services

• Technology used in IT systems for all components interacting with RtP, and the focus on the

existing implementation for fund transfer management (ordinary SCT, SCT Inst and other

transfers)

• Consequence on interactions between existing components and those that will be executed,

mainly between RtP and payment - depending also on either a very urbanized approach,

segmenting the role per components, or an integrated approach, dealing with end-to-end RtP

and all the necessary functions in one component

• Opportunity not to change applications of IT systems and even entrust the management of

RtP to a service provider

• Other ongoing or upcoming projects impacting the payment sector (EPC’s regulatory

production, or EPI project for a retail European payment scheme)

Each stakeholder would have to adapt its implementation strategy according to its IT system.

Indeed, the reuse of all or part of certain components can be useful and result in cost savings. Hence,

investments can be optimized in order to assign to those services with higher-added value for

clients, therefore generating more revenue.

4.3. Implementation challenges to overcome

Request-to-Pay solutions can provide a range of different services; for instance, a receipt displayed in

a digital wallet with “Pay Now” and “Pay Later” buttons; a notification at the physical point of sale

that the funds have reached the merchant or notification and initiation of the next payment in a

conveyance chain. Nevertheless, several difficulties need to be addressed in terms of implementation,

such as:

• Front-end channels to be set up according to each client’s segment and depending on the

products’ distribution and the client’ path

• Life cycle of business functions for Request-to-Pay and payment ensuring overall cohesion:

management of the reconciliation between RtP and Payment, synchronization between the

two, links in case of dispute...

• High availability and reactivity according to each use case, optimizing resources (avoids

oversizing or undersizing of technical infrastructures). The difficulty for this new service is to

33

082010 - White paper Galitt – Request-to-Pay

estimate the volumes to be processed, in number as well as size. In fact, an RtP can carry

several attachments, the size of which is not standardized

The two additional implementation challenges are linked to the capacity to process and communicate

rapidly between different actors. It is also necessary to know how to manage necessary

synchronization situations between RtP and payment when the transaction fails. It is, therefore,

necessary to implement better processes for security and resiliency.

PSPs have a unique advantage in terms of customer trust and access within the payments ecosystem.

PSPs that take advantage of Request-to-Pay’s potential are better positioned to serve their

customers, both from a business and a consumer perspective. Moreover, providing an RtP solution

and making new channels available to their customers will be an additional advantage of the offers

but will require less effort, particularly because of the sensitive subject of their access security.

Urbanized distribution of banking functions and links with large corporate customers (high-level

vision)

From a technical and organizational point of view, PSPs have teams and infrastructures used for

initiation, execution, payment transfer and payment management. Moreover, they have developed

banking communication channels (SWIFT, EBICS, Web-banking, API, etc.) adapted to different types

of clients. This allows them to rely on a solid competence and existing components, having benefited

from their long experience in the payment sector. Although not perfect, PSPs can rely on their vision

of optimized repartition of IT system functions and their component software, knowing how to

combine those complementary features.

34

082010 - White paper Galitt – Request-to-Pay

Conclusion

RtP has the potential to be the missing link in the European payments market, changing the entire

landscape as we know it. There is no doubt that RtP will increase the convenience of paying and

receiving money while reducing the friction and cost of collections. In particular, RtP holds the key to

unlocking the significant potential that instant payment has to offer, both for consumers and

businesses.

In addition, with most Request-to-Pay enablers already in place, PSPs and other players can take

advantage of existing investments in infrastructure and SEPA systems to become significantly more

agile and innovative, by providing long-term payment products and services with the perspective of

the European Payment Initiative (EPI). Backed by the European decision-maker with an ambitious

agenda, EPI has reached the project implementation stage. While development and roll-out are yet

to be planned, EPI namely relies on RtP for several of its features.

Meeting market needs better than ever before for C2B and B2B use cases, as well as catering for a

large consumer acceptance and adoption, this new payment link is promised to become a corner-

stone of Europe’s, and maybe the global, economy.

35

082010 - White paper Galitt – Request-to-Pay

About the authors

Emmanuel CARON – Practice Manager, Regulation & Economics (Galitt)

“With 20 years of experience in European card markets and payment systems/schemes,

Emmanuel is currently leading two consulting practices within Galitt: Payment

Regulation and Business Models. His recent areas of intervention cover regulatory

issues like PSD2, EBA standards, as well as addressing the challenge of Open Banking

for financial institutions, fintechs and e-merchants. He has the responsibility to deliver

cross-EU business model analysis and strategic and regulatory impact assessments for

banks, payment schemes, payment service providers and merchants. He also

moderates Galitt payment education sessions on European payment markets, both

card and SEPA instruments.”

Guillaume DE LONGEAUX – Manager, Retail Payments & Public Affairs

(Galitt)

“A Manager at Galitt since 2017, Guillaume is trilingual and enjoys a 20-year experience

in retail payments and compliance management. He implements the company’s

expansion in emerging services combining SEPA, open banking and cash management:

instant payment, card/transfer mix, seamless Strong Authentication. A Sciences Po

Paris graduate, Guillaume advises financial institutions in Public Affairs as well:

lobbying, interbank cooperation, regulatory authorisations. He also delivers Galitt’s

training courses on SEPA payments and on card markets in Europe, thanks to his early

career at French Groupement des Cartes Bancaires CB.”

Jules BE KUTI – Economics & Regulatory Consultant (Galitt)

“

Jules is involved in opportunity and feasibility studies related to the regulation and

transformation of the payments market in Europe. Jules has also worked on regulatory

compliance issues such as internal control, gap analysis and remediation plan.”

Hugues LECLÈRE – Product Strategy Manager, Payment Product Strategy

(Sopra Banking Sotware)

“In the world of Software for thirty years, Hugues has developed his experience by

working closely with customers, banks and corporates, and by building Sofware within

R&D teams. He is now Product Manager within the Payment Product Stategy teams in

Sopra Banking Software.”

36

082010 - White paper Galitt – Request-to-Pay

Several other contributors have made this project possible:

Rémi Gitzinger – Executive Director, Galitt

Hélène Kalem – Practice Manager, Galitt

Diane Ribeiro – Payment Consultant, Galitt

Cécile Rouhaud – Benchmark Observatory, Galitt

Valérie Bellec – Product marketing, payments, Sopra Banking Software

Will Kitson – Head of content and research, Sopra Banking Software