1

The IRS Ceased Compliance With the $10 Million

Taxpayer Treasury Directive in Favor of an Overall Focus

on High-Income Taxpayer Noncompliance

June 20, 2024

Report Number: 2024-300-028

TIGTACommunic[email protected]eas.gov | www.tigta.gov

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

HIGHLIGHTS: The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Final Audit Report issued on June 20, 2024 Report Number 2024-300-028

Why TIGTA Did This Audit

This audit was initiated to

determine whether the IRS is

meeting the former Secretary of

the Treasury’s established goal

requiring the IRS to audit a

minimum of 8 percent of all high-

income individual returns, with

incomes more than $10 million,

filed each year.

On February 10, 2020, the then

Secretary of the Treasury directed

the IRS, pursuant to 26 United

States Code Sections 7801 and

7803(a)(2), to audit a minimum of

8 percent of all high-income

individual returns filed each year.

On March 13, 2020, the IRS

Commissioner responded that

accomplishing the goal would

require significant opportunity

costs but agreed to comply using

total positive income of $10 million

or more to select returns (2020

Treasury Directive).

In August of 2022, the Inflation

Reduction Act was enacted with

the purpose in part to fund the IRS

so that it could examine more

high-income taxpayers. In an

August 2022 directive to the IRS,

the Secretary of the Treasury

directed that no Inflation

Reduction Act funding should be

used to increase the audit rate of

taxpayers with incomes below

$400,000 (2022 Treasury Directive).

Impact on Tax Administration

An analysis of the 2020 Treasury

Directive assists in understanding

the impact on audit productivity

that comes from focusing audit

resources on taxpayers above

certain high-income thresholds.

What TIGTA Found

The IRS complied with the 2020 Treasury Directive for three tax years

but ceased monitoring it at the end of Fiscal Year 2023. At the start

of this audit, an IRS executive informed TIGTA in December of 2022

that the 2020 Treasury Directive would no longer be followed

because these audits were unproductive having high no-change

rates. The IRS also stated it was embarking on a different approach

focusing on complying with the 2022 Treasury Directive.

TIGTA found that many of the examined returns pursuant to the 2020

Treasury Directive were productive depending on which IRS function

conducted the examinations and which case selection methods

were used. The Small Business/Self Employed Division’s closed

examinations of individual taxpayer returns with income of

$10 million or more, in Tax Years 2016 through 2021, were generally

more productive than income ranges below $10 million, yielding

four times more dollars assessed per return and two times more

dollars assessed per hour when compared to examinations of returns

with income of $400,000 to under $10 million.

On the other hand, Large Business and International Division case

selection methods in place prior to the 2020 Treasury Directive

resulted in better productivity metrics when compared to

post-Treasury Directive results. For example, the no-change rate has

increased when comparing pre-directive tax years (Tax Years 2016

through 2017) to post-directive tax years (Tax Years 2018 through

2020).

TIGTA also found that some of the opportunity costs the IRS

identified in response to the Department of the Treasury at the

outset of the 2020 Treasury Directive were overstated by

190 examinations of large and mid-sized businesses.

What TIGTA Recommended

TIGTA made two recommendations to the IRS: (1) include a separate

category for taxpayers with TPI of $10 million or more when

evaluating the compliance of high-income individual taxpayers for

Initiative 3.4 of the IRS Strategic Operating Plan to ensure the

productivity of examinations on these high-income individual returns

are tracked and analyzed in comparison to examinations of taxpayers

at other income levels; (2) identify the potential causes for the Large

Business and International Division’s low productivity examination

results and monitor measures to ensure that the most productive

returns are selected for examination.

The IRS partially agreed with both recommendations stating that it

already categorizes and monitors productivity measures for

high-income high-wealth taxpayers, including those with TPI of $10

million or more, and that it will identify the potential causes for the

low productivity examination results and will use enhanced data and

analytics to select cases based on the highest risk of noncompliance.

U.S. DEPARTMENT OF THE TREASURY

WASHINGTON, D.C. 20024

TREASURY INSPECTOR GENERAL

FOR TAX ADMINISTRATION

June 20, 2024

M

EMORANDUM FOR: COMMISSIONER OF INTERNAL REVENUE

F

ROM:

SUBJECT:

Matthew A. Weir

Acting Deputy Inspector General for Audit

Final Audit Report – The IRS Ceased Compliance With the $10 Million

Taxpayer Treasury Directive in Favor of an Overall Focus on

High-Income Taxpayer Noncompliance (Audit No.: 202330020)

This report presents the results of our review to determine whether the Internal Revenue Service

(IRS) was meeting the Department of the Treasury’s established goal of auditing a minimum of

8 percent of all high-income individual returns filed each year.

1

This review was part of our

Fiscal Year 2023 Annual Audit Plan and addresses the major management and performance

challenge of

Increasing Domestic and International Tax Compliance and Enforcement

.

Management’s complete response to the draft report is included as Appendix V. If you have any

questions, please contact me or Phyllis Heald London, Acting Assistant Inspector General for

Audit (Compliance and Enforcement Operations).

1

Our audit focused on IRS examinations of individual returns with total positive income of $10 million or more, which

the IRS used to comply with the minimum 8 percent audit rate goal.

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Table of Contents

Background .....................................................................................................................................Page 1

Results of Review .......................................................................................................................Page 3

The IRS Achieved Compliance With the 2020 Treasury

Directive for Three Tax Years Until Compliance Was

Terminated .............................................................................................................................Page 3

The Small Business/Self-Employed Division’s

Examinations of Individual Returns of Taxpayers Earning

$10 Million or More Have Generally Been More

Productive Than Returns Examined at Lower Income

Levels ........................................................................................................................................Page 5

Recommendation 1: ...................................................................Page 8

The Large Business and International Division’s Selection

Methods for Returns Examined as Part of the 2020

Treasury Directive Need Improvement ........................................................................Page 9

Recommendation 2: ...................................................................Page 13

The IRS Overstated the Opportunity Costs Associated

With the 2020 Treasury Directive ...................................................................................Page 14

Appendices

Appendix I – Detailed Objective, Scope, and Methodology ................................Page 16

Appendix II – Secretary of the Treasury Steven Mnuchin’s

February 10, 2020, Directive to IRS Commissioner Charles Rettig ....................Page 18

Appendix III – IRS Commissioner Charles Rettig’s March 13, 2020,

Response to Secretary of the Treasury Steven Mnuchin’s

February 10, 2020, Directive .............................................................................................Page 19

Appendix IV – Secretary of the Treasury Janet Yellen’s

August 10, 2022, Directive to IRS Commissioner Charles Rettig .......................Page 23

Appendix V – Management’s Response to the Draft Report ..............................Page 25

Appendix VI – Glossary of Terms ...................................................................................Page 29

Appendix VII – Abbreviations ..........................................................................................Page 30

Page 1

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Background

On February 10, 2020, the Secretary of the Treasury issued a memorandum to the Internal

Revenue Service (IRS) Commissioner directing the IRS, pursuant to 26 United States Code

Sections 7801 and 7803(a)(2), to take all steps necessary to audit a minimum of 8 percent of all

high-income individual returns filed each year, starting with Tax Year (TY) 2016 (hereafter

referred to as the 2020 Treasury Directive).

1

The 2020

Treasury Directive also defined “high-income individual

returns” as individual tax returns with adjusted gross

income in excess of $10 million.

2

In this

communication, the Secretary also stressed that,

“Robust enforcement of the tax laws is critical to

ensuring fairness in our tax system. By pursuing

taxpayers who fail to comply with their tax obligations

the IRS treats compliant taxpayers fairly and

incentivizes all taxpayers to voluntarily comply with the

law.

” The IRS has traditionally categorized taxpayers

with total positive income (TPI) of $200,000 or more as

“high-income” taxpayers, which has not been updated

since June 2006. In multiple reports, the Treasury Inspector General for Tax Administration

(TIGTA) has recommended that the IRS reevaluate its threshold for what it considers

high-income taxpayers.

3

The IRS agreed to study TIGTA’s recommendation in 2015, but as

recently as 2023 disagreed with TIGTA’s recommendation to increase the dollar threshold for

what constitutes high-income taxpayers.

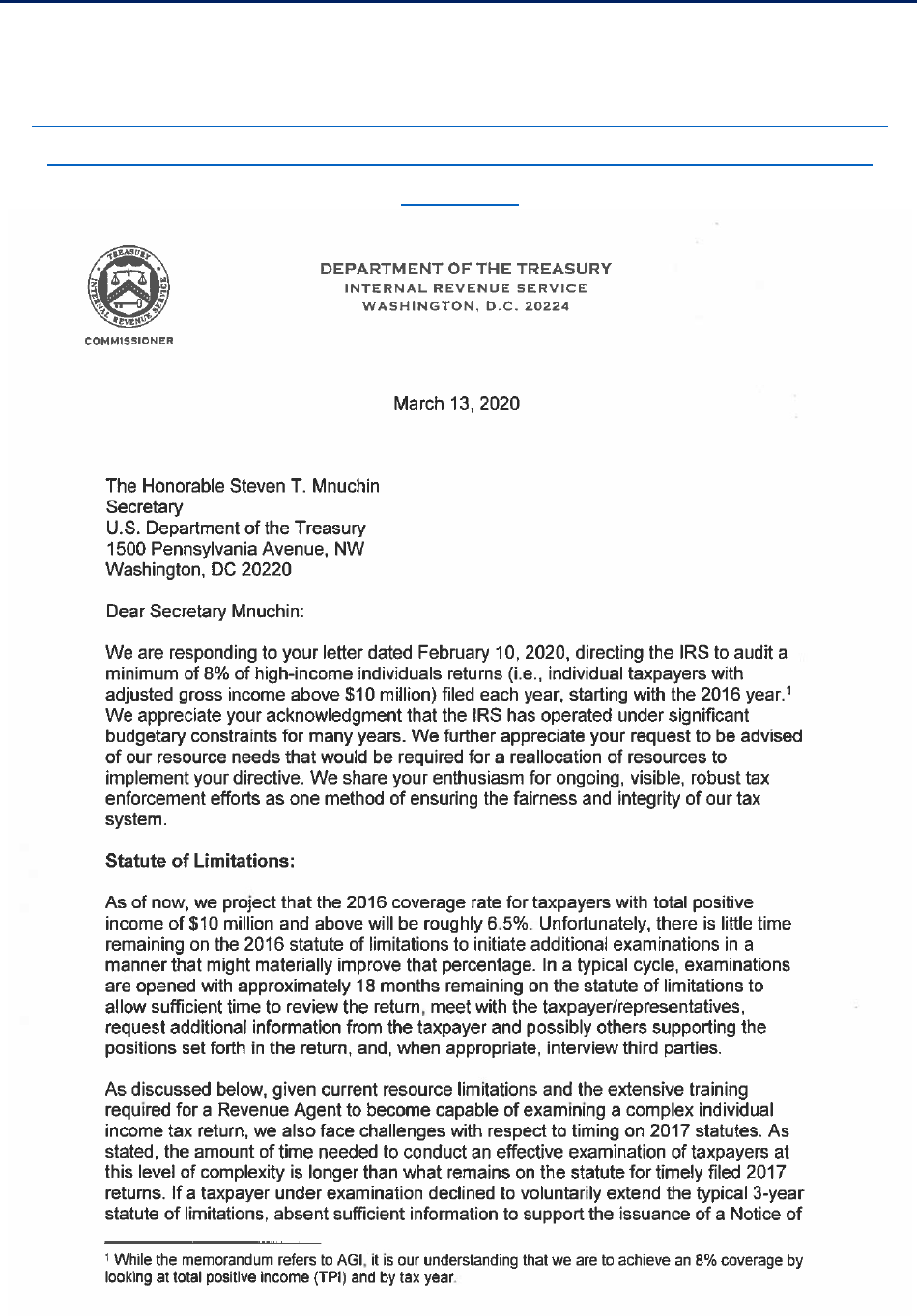

On March 13, 2020, then IRS Commissioner Charles Rettig provided a response to the Secretary

of the Treasury’s February 2020 Treasury Directive stating that the IRS would use TPI of

$10 million or more to select returns.

4

The Commissioner expressed various limitations and

trade-offs to comply with the 2020 Treasury Directive. First, the assessment statute of

limitations is generally three years from the date a return is filed, and therefore, the IRS would

generally be prevented from examining TYs 2016 and 2017.

5

New examinations are usually

opened with more than 18 months remaining on the statute of limitations to allow sufficient

time for an audit to be completed. For TY 2016, the IRS’s projected coverage rate for taxpayers

with TPI of $10 million or more would be around 6.5 percent because there was little time

remaining on the TY 2016 statute of limitations to initiate additional examinations in a manner

1

Correspondence, Secretary of the Treasury Steven Mnuchin to IRS Commissioner Charles Rettig. (Feb. 10, 2020).

See Appendix II. Generally, the tax year is synonymous with the calendar year. See Appendix V for a glossary of

terms.

2

Adjusted gross income, in the case of an individual, means gross income minus certain deductions and losses listed

in Internal Revenue Code Section 62(a).

3

TIGTA, Report No. 2015-30-078,

Improvements Are Needed in Resource Allocation and Management Controls for

Audits of High-Income Taxpayers

(Sept. 2015); TIGTA, Report No. 2023-30-054,

The IRS Needs to Leverage the Most

Effective Training for Revenue Agents Examining High-Income Taxpayers

(Aug. 2023).

4

Correspondence, IRS Commissioner Charles Rettig to Secretary of the Treasury Steven Mnuchin. (Mar. 13, 2020).

See Appendix III.

5

Internal Revenue Code Section 6501(a).

“

Robust enforcement of the tax

laws is critical to ensuring

fairness in our tax system. By

pursuing taxpayers who fail to

comply with their tax

obligations, the IRS treats

compliant taxpayers fairly and

incentivizes all taxpayers to

voluntarily comply with the law

.”

Page 2

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

that might materially improve that percentage. Similar challenges were referenced in meeting

the audit rate for examinations of TY 2017 tax returns.

Second, was the need for additional resources and the opportunity costs associated with

complying with the 2020 Treasury Directive, suggesting that achieving and maintaining an

8 percent audit rate for high-income individuals would require:

• More resources of at least 400 full-time revenue agents, with the majority being at the

General Schedule Grade 13 level;

6

and

• Opportunity costs consisting of 900 fewer audits of large and mid-size business returns,

600 fewer audits of small corporate returns and 850 fewer audits of individual returns

with TPI under $10 million.

The Small Business/Self-Employed (SB/SE) Division and the Large Business and International

(LB&I) Division conduct the audits of higher income taxpayers, including those of individual

returns with TPI of $10 million or more (hereafter referred to as “$10 million or more income”

returns/audits). The IRS initially split the responsibility equally for complying with the 2020

Treasury Directive between the SB/SE and LB&I Divisions; however, because the LB&I Division’s

resources were limited due to other work, the allocation shifted starting with TY 2019 returns

selected for examination so that the SB/SE Division would be responsible for two-thirds and the

LB&I Division would be responsible for one-third of the audits.

7

As such, both divisions play a

critical role in the IRS’s compliance with the 2020 Treasury Directive.

In August 2022, the Inflation Reduction Act of 2022 was enacted, providing $79.4 billion (in

addition to other funds made available) to the IRS over a decade.

8

Congress allocated

$45.6 billion of Inflation Reduction Act funding towards enforcement activities. Through

multiple subsequent recissions, these amounts were reduced to $57.8 billion and $24 billion,

respectively.

9

As the Secretary of the Treasury wrote to the then IRS Commissioner in August of

2022, Inflation Reduction Act enforcement funding was intended in part to increase

examinations of high-income taxpayers (hereafter referred to as the 2022 Treasury Directive).

The Secretary stated:

Specifically, I direct that any additional resources—including any new personnel or

auditors that are hired—shall not be used to increase the share of small businesses or

households below the $400,000 threshold that are audited relative to historical levels.

6

Revenue agents at the General Schedule Grade 13 level are highly trained and are knowledgeable in the full range

of tax issues, accounting systems, and tax compliance programs relative to conducting Federal tax examinations. A

GS-13 revenue agent in the Large Business and International Division will work on cases involving individuals and

business organizations that may include extensive subsidiaries with operations of national and/or international scope,

while a GS-13 revenue agent in the Small Business/Self-Employed Division will work on cases involving returns filed

by individuals, small businesses, organizations, and other entities.

7

TIGTA, Report No. 2023-30-054,

The IRS Needs to Leverage the Most Effective Training for Revenue Agents

Examining High-Income Taxpayers,

p. 10 (Aug. 2023). At the end of Fiscal Year (FY) 2020 there were 4,215 revenue

agents in SB/SE and 3,062 in LB&I. As of March 31, 2023, there were 4,227 revenue agents in SB/SE and 2,908 in LB&I.

8

Pub. L. No. 117-169, 136 Stat. 1818.

9

Congress subsequently rescinded approximately $1.4 billion in IRA funding with Section 251 of the Fiscal

Responsibility Act of 2023, Pub. L. No. 118-5, and an additional $20.2 billion with Sections 530 and 640 of the Further

Consolidated Appropriations Act, 2024, Pub. L. No. 118-47;

i.e.

, a total $21.6 billion reduction in funding and

allocation to enforcement activities.

Page 3

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

This means that ... small businesses or households earning $400,000 per year or less will

not see an increase in the chances that they are audited.

Instead, enforcement resources will focus on high-end noncompliance. There, sustained,

multiyear funding is so critical to the agency’s ability to make the investments needed to

pursue a robust attack on the tax gap by targeting crucial challenges, like large

corporations, high-net-worth individuals and complex pass-throughs, where today the

IRS has resources to initiate just 7,500 audits annually out of more than 4 million returns

received

.

10

At the initiation of this audit in December 2022, the acting Deputy Commissioner for Services

and Enforcement informed TIGTA that the IRS was no longer going to pursue the 2020 Treasury

Directive because the examinations were unproductive. For example, many of the cases

examined under the directive had high “no-change” rates (meaning that there was a high

percentage of examinations that did not result in a change to the amount of tax due).

Results of Review

The IRS Achieved Compliance With the 2020 Treasury Directive for Three Tax

Years Until Compliance Was Terminated

Both the SB/SE and LB&I Divisions were responsible for completing and monitoring audits to

reach the targeted audit rate; however, the SB/SE Division was responsible for preparing the

official audit rate reports for the 2020 Treasury Directive.

11

Due to the statute of limitations

issues previously cited, the IRS started to address the 2020 Treasury Directive audit goal with

TY 2018. However, since the 2020 Treasury Directive requested the IRS to apply the audit rate

goal starting with TY 2016, we included TYs 2016 and 2017 in our review. As such, the IRS

provided TIGTA its monitoring reports including information on the in-process and completed

audits through September 30, 2023, for TYs 2018 through 2021. Figure 1 presents the audit rate

metrics for TYs 2016 through 2021.

12

10

Correspondence, Secretary of the Treasury Janet Yellen to IRS Commissioner Charles Rettig. (Aug. 10, 2022). See

Appendix IV.

11

The SB/SE Division was responsible for preparing the

Audit Rate $10M Monitoring Report

, which monitored the

IRS’s agencywide opened and closed examinations against the total filed returns by tax period for individual taxpayers

with TPI of $10 million or more. The IRS used this report to monitor the 2020 Treasury Directive 8 percent audit rate

goal.

12

The IRS did not provide a breakdown of the audits in process or closed for TYs 2016 and 2017, so this information

was obtained from Table 17 of the IRS Data Book, 2022.

Page 4

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Figure 1: IRS Audit Rates for Individual Tax Return Examinations

With TPI of $10 Million or More for TYs 2016 Through 2021

13

Source: TIGTA’s analysis of closed and open tax return examinations as of September 30, 2023, per IRS

Monitoring Reports and the IRS Data Book, 2022.

As illustrated in Figure 1, the IRS did not meet the 2020 Treasury Directive goal for TYs 2016 or

2017. As of September 30, 2023, the audit rate for TY 2016 was slightly under 8 percent

(exceeding the then Commissioner’s estimated 6.5 percent audit rate for TY 2016) and

approximately 6 percent for TY 2017. However, the IRS exceeded the 8 percent audit rate goal

(based on the 2020 Treasury Directive) for TYs 2018 through 2020. As of September 30, 2023, it

was still too early to determine the TY 2021 audit rate for the $10 million or more income

earning taxpayers since the tax year is considered open.

In response to the 2020 Treasury Directive, the IRS established additional activity codes used to

track taxpayers earning $10 million or more. In January 2022, the IRS created additional activity

codes to track returns with TPI of $10 million or more. Prior to January 2022, Activity Code 281

was used to track Forms 1040,

U.S. Individual Income Tax Return

, with TPI of $1 million or more.

As part of the activity code revisions, the TPI range covered by Activity Code 281 was split into

three activity codes. One of the three, was Activity Code 284 that was created to track Forms

1040 (individual taxpayers) with TPI of $10 million or more.

As of September 30, 2023, the IRS completed 7,688 examinations of individual returns with TPI

of $10 million or more for TYs 2016 through 2021.

The IRS no longer has a target audit rate in place for examinations of individual returns

with TPI of $10 million or more

In February 2023, IRS executives informed TIGTA that the IRS would continue to audit

high-income individual returns with TPI of $10 million or more but would not aim to achieve

the 8 percent audit rate in the future. IRS executives stated at that time that they considered the

2020 Treasury Directive obsolete. The executives explained that the IRS’s new focus will be on

compliance with the 2022 Treasury Directive to expand examinations of individuals with incomes

of $400,000 or more. In November 2023, the SB/SE Division informed TIGTA that it would no

13

The SB/SE and LB&I Divisions are currently in the process of auditing returns for TYs 2016 through 2021, so values

for these TYs are subject to change. Furthermore, the IRS did not provide a breakdown of the audits in process or

closed for TYs 2016 and 2017 and applied the 2020 Treasury Directive audit rate goal starting with TY 2018.

Page 5

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

longer generate the agencywide

Audit Rate $10M Monitoring Report

and that the last report

prepared was through the end of FY 2023. Therefore, the IRS no longer monitors whether it has

met or needs to put in process additional examinations to meet, the 8 percent audit rate goal

established by the 2020 Treasury Directive for high income individuals with TPI of $10 million or

more.

On April 5, 2023, the IRS issued Publication 3744,

Inflation Reduction Act Strategic Operating

Plan

(hereafter referred to as Strategic Operating Plan) for FYs 2023 to 2031. IRS management

stated that the Strategic Operating Plan was designed to be a framework on how the IRS will

meet the new 2022 Treasury Directive. While the Strategic Operating Plan includes the

expansion of enforcement surrounding high-income high-wealth individuals, the elimination of

its 2020 Treasury Directive audit rate makes it unclear the extent to which the IRS plans to audit

these high-income individual tax returns.

The Strategic Operating Plan includes initiatives to address high-dollar compliance issues, such

as those related to high-income individuals, however, the initiatives do not define high-income

individuals or establish any target audit rates or goals. While the SB/SE Division confirmed that

it would no longer monitor and report the $10 million or more high-income audit rates, it did

communicate that certain case metrics can be evaluated to determine performance of audits,

regardless of whether a target audit rate is provided,

i.e.

, no change rate, dollars recommended

per return/hour, average returns per case, average hours per case, days per return, average case

length, and return pick-up rate. However, goals are not associated with these measures.

IRS management informed TIGTA that their FY 2024 Enterprise-wide Examination Plan outlines

the planned starts for return examinations including those for individuals with TPI of $10 million

or more, which they consider are clear and measurable goals. However, according to the IRS,

the FY 2024 Enterprise-wide Examination Plan has not been finalized and the planned return

examination starts are subject to change. IRS management informed us they are reviewing

FY 2024 first and second quarter examination data to help determine the number of starts they

will need for the rest of the fiscal year.

Achieving a goal of planned new examination “starts” alone, may not allow for the IRS to identify

and work the most egregious highest income returns and could cause Inflation Reduction Act

funds for audits of high-income individual returns to be used inefficiently. For example,

achieving 100 percent of planned examination starts may satisfy the goal; however, if most of

these examinations were closed as no-change, the limited IRS resources would be expended

examining returns of compliant taxpayers who would be unnecessarily burdened.

The Small Business/Self-Employed Division’s Examinations of Individual

Returns of Taxpayers Earning $10 Million or More Have Generally Been More

Productive Than Returns Examined at Lower Income Levels

The SB/SE Division’s management established a Compliance Initiative Project (CIP) to comply

with the 2020 Treasury Directive and at the end of the CIP found that the results justified the

time and resources spent on auditing high-income returns. Furthermore, our analysis of the

SB/SE Division’s closed examinations of individual taxpayers with TPI of $10 million or more, for

TYs 2016 through 2021, as of June 30, 2023, were more productive than TPI ranges of $400,000

to under $10 million. For the six years, the SB/SE Division assessed over $574 million, averaging

Page 6

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

approximately $124,389 per return and approximately $2,220 per hour for individual returns

with TPI of $10 million or more.

14

The Government Accountability Office’s,

Standards for Internal Control in the Federal

Government

,

provides “monitoring” as one of the five components for internal control.

15

Monitoring provides that management should establish and operate monitoring activities to

assess the quality of performance and promptly take corrective actions to achieve objectives.

To monitor and evaluate noncompliance,

the IRS typically uses productivity

measures including, but not limited to,

the average dollars assessed per return

and the average dollars assessed per

hour. The IRS calculates the average

dollars assessed per return by dividing

the sum of the total positive dollars

recommended for each audit by the

number of closed audits. Similarly, the

IRS calculates the average dollars

assessed per hour by dividing the sum of

the total positive dollars recommended

for each audit by the number of hours

spent on these audits. All audits that

result in a refund would be reported as

zero when calculating the total dollars

assessed. We used the IRS’s

methodology in analyzing the data, and

the results of our analysis are presented

in Figures 2 and 3.

Using the Audit Information Management System – Centralized Information System (A-CIS)

closed case data for TYs 2016 through 2021 returns, we calculated and analyzed the average

dollars assessed per return and the average dollars assessed per hour for the SB/SE Division, as

of June 30, 2023.

16

For TY 2016 through 2021, Figure 2 compares the average dollars assessed per return for returns

with TPI of $10 million or more to returns with TPI of $400,000 to under $10 million.

Examinations of returns with TPI of $10 million or more yielded four times more dollars assessed

per return for TYs 2016 through 2021 when compared to the dollars assessed per return for

returns with TPIs of $400,000 to under $10 million.

14

The amount assessed is the sum of the total positive dollars recommended. Therefore, all return examinations that

result in a refund would be reported as zero. The average assessment was calculated using the cumulative total

positive dollars divided by the total returns examined, including returns resulting in a no change or refund.

15

Government Accountability Office, GAO-14-704G,

Standards for Internal Control in the Federal Government

, p.64

(Sept. 2014).

16

SB/SE Division has active exams open/in process for TYs 2016 through 2021, so values for those tax years are

subject to change.

Figure 2: Examinations of Returns with TPI

$10 Million or More Yield 4 Times More Dollars

Assessed per Return.

Source: TIGTA’s analysis of closed tax return

examinations as of June 30, 2023, per A-CIS data

provided by the IRS.

Page 7

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

For TYs 2016 through 2021, Figure 3

compares the average dollars assessed per

hour for examinations of returns with TPI

of $10 million or more to returns with TPI

of $400,000 to under $10 million.

Examinations of returns with TPI of

$10 million or more yielded two times

more dollars assessed per hour for

TYs 2016 through 2021 when compared to

the dollars assessed per hour for returns

with TPIs of $400,000 to under $10 million.

These productivity measures are indicators

that audits of individual returns with TPI of

$10 million or more are more productive

than the TPI ranges shown below

$10 million.

Our analysis of the average dollars

assessed per return and per hour at the

various TPI ranges shows that the SB/SE

Division examinations of returns with TPI of

$10 million or more are more productive than returns with the lower TPI ranges reviewed by

TIGTA. SB/SE management stated that this is because returns with TPI of $10 million or more

tend to have larger issue adjustments and therefore higher recommended tax amounts.

The SB/SE Division’s CIP for the 2020 Treasury Directive was open for approximately three years

and ended in June 2023. The CIP covered selections for TYs 2018 through 2020 and assisted the

SB/SE Division in meeting its share of the 2020 Treasury Directive audit rate requirement, not

covered by examinations selected under other workstreams.

17

On September 26, 2023, the

SB/SE Division issued the CIP Termination Report, detailing the results of the audits of

high-income tax returns. The report stated that there was a total of 1,761 returns examined

under this CIP, of which approximately 25 percent (442 returns) resulted in a no change.

Revenue agents averaged 68 hours to complete each return examination with an average

deficiency of $65,483 and an average of $957 dollars per hour. The IRS has determined that,

based on the results of the CIP, it will continue to address the noncompliance of taxpayers who

filed high-income returns. The IRS believes that the CIP results justified the time and resources

spent on auditing high-income returns. Additionally, the SB/SE Division has partnered with the

Research, Applied Analytics, and Statistics Division to analyze the population of taxpayers who

file these high-income returns to identify areas of noncompliance, so that it can better

determine how to address noncompliance in this population. By selecting returns that are more

productive,

i.e.

, returns resulting in a tax assessment and therefore non-compliant, the SB/SE

Division will also reduce the burden placed on the taxpayers who are more compliant.

In response to an earlier TIGTA audit, the IRS agreed to establish an enterprise examination plan

rather than having the four IRS Operating Divisions establish their own goals, each with their

17

A workstream is a type or category of work, such as the Discriminant Index Function, where returns are selected for

audit based on their computer-scored examination potential.

Figure 3: Examinations of Returns with TPI

$10 Million or More Yield 2 Times More Dollars

Assessed per Hour

Source: TIGTA’s analysis of closed tax return

examinations as of June 30, 2023, per A-CIS data

provided by the IRS.

Page 8

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

own priorities.

18

The IRS is currently in the process of developing a unified examination plan for

the first time. The IRS has also announced a new organizational structure which will further

impact accountability for examination operations.

19

The Strategic Operating Plan does not address the 2020 Treasury Directive required audit rate,

but it does state that the IRS intends to increase enforcement activities to help ensure tax

compliance of high-income high-wealth individuals. However, the Strategic Operating Plan

does not define “high-income” or “high-wealth” individuals. As outlined in Initiative 3.4 of its

Strategic Operating Plan, the IRS intends to use data and analytics to improve their

understanding of tax filings of high-wealth individuals and to pursue noncompliance through a

variety of mechanisms, including audits and non-audit contacts. Success for this initiative

includes an increase in the audit coverage rates and other types of enforcement of high-income

high-wealth taxpayers to improve voluntary compliance. The IRS informed TIGTA that it is in the

process of working on definitions related to Initiative 3.4 of the Strategic Operating Plan. Until

the IRS completes its new process on high-income individual taxpayers at all levels including

taxpayers with TPI of $10 million or more, TIGTA will continue to direct recommendations

pursuant to the existing IRS structure.

Recommendation 1: The Deputy Commissioner, Services and Enforcement, should include a

separate category for taxpayers with TPI of $10 million or more when evaluating the compliance

of high-income individual taxpayers for Initiative 3.4 of the IRS Strategic Operating Plan to

ensure the productivity of examinations on these high-income individual returns is tracked and

analyzed in comparison to examinations of taxpayers at other income levels.

Management’s Response: The IRS partially agreed with this recommendation stating it

has already categorized taxpayers at multiple TPI amounts and monitors productivity

measures related to high-income high-wealth taxpayers, including those with TPI of

$10 million or more, to ensure the most productive returns are selected for examination.

The IRS agrees with TIGTA’s goal of evaluating the compliance of all high-income

high-wealth taxpayers; however, the IRS disagreed that it should compare specific levels

of TPI.

Office of Audit Comment: As part of its commitment to the 2022 Treasury

Directive to not increase audit rates for taxpayers making under $400,000, the IRS

should review and compare the productivity for high-income taxpayers

exceeding this threshold at various ranges. The factors used to identify the most

productive returns at the lower end ($400,000 level) may be quite different than

those related to the highest income taxpayers including those with TPI of

$10 million or more.

18

TIGTA, Report No. 2023-30-008,

Opportunities Exist for the IRS to Develop a More Coordinated Approach to

Examination Workplan Development and Resource Allocation

(Feb. 2023).

19

IR-2023-237,

New Structure Features Single Deputy IRS Commissioner, Four Chief Executive Positions to Cover

Taxpayer Service, Compliance, IT and Operations

(Dec. 13, 2023).

Page 9

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

The Large Business and International Division’s Selection Methods for

Returns Examined as Part of the 2020 Treasury Directive Need Improvement

LB&I case selection methods in place prior to the 2020 Treasury Directive resulted in better

productivity metrics when compared to post-Treasury Directive results. Like the SB/SE Division,

the LB&I Division started to address the 2020 Treasury Directive audit goal with TY 2018. For

TYs 2016 and 2017, an individual return would be opened as part of a related business return

examination, when known adjustments were required to be made at the individual return level.

For the LB&I Division to achieve their designated portion of the 2020 Treasury Directive audit

rate going forward, management needed to use other selection methods.

Prior to the 2020 Treasury Directive, the LB&I Division’s individual returns were generally either:

1) international returns where the taxpayers generally had reported income under $200,000, or

2) returns that were picked up for review based on an associated business return that was

already selected for examination as part of the Global High Wealth (GHW) program.

20

As a

result of the 2020 Treasury Directive, the LB&I Division modified its GHW selection methodology

to identify individual taxpayers with TPI of $10 million or more.

21

The modified GHW model, is

referred to as the High-Income Individual (HII) model and was used by the division for TYs 2018

through 2020.

22

LB&I management explained that in addition to the GHW and HII models, their

division used other selection methods to select individual returns for the 2020 Treasury Directive

audits.

To monitor and evaluate noncompliance, the IRS typically uses productivity measures including

the no change rate, the average dollars assessed per return and the average dollars assessed per

hour. Using the A-CIS closed case data for individual returns as of June 30, 2023, we calculated

and analyzed the three productivity measures for the LB&I Division using the same TPI ranges

applied to the SB/SE Division. We found that there was no TPI range consistently more

productive, including individual returns with TPI of $10 million or more.

As a result of this inconclusive analysis, we further analyzed the LB&I Division’s TY 2016 through

TY 2021 closed case data for individual returns with TPI of $10 million or more, as of

June 30, 2023, by selection method and compared the productivity measures for cases selected

by:

• GHW Model – Returns selected under this model impacted TYs 2016 through 2020

return case selections.

• HII Model – This model was implemented because of the 2020 Treasury Directive and

impacted TYs 2018 through 2020 return case selections.

20

TIGTA, Report No. 2023-30-019,

The IRS Large Business and International Division Should Consider Shifting

Individual Examination Resources to More Productive Examinations

(May 2023). In this report, TIGTA found that most

LB&I individual returns are taxpayers with reported incomes below $200,000. The GHW program takes a holistic view

of an individual income tax return by looking at their entire financial picture and the enterprises they control.

21

In December 2019, the LB&I Division used the GHW model to select individual TY 2018 returns for examination.

However, in response to the 2020 Treasury Directive, the LB&I Division reselected its TY 2018 individual returns in

March 2020 using the modified GHW model.

22

For TY 2021, the LB&I Division moved to a selection method called the Artificial Intelligence Risk model to identify

individual taxpayer returns with TPI of $10 million or more. However, as of our analysis on June 30, 2023, there were

no closed returns from this selection method.

Page 10

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

• Other – All other selection methods were combined under this category.

23

As of June 30, 2023, for TYs 2016 through 2021, the LB&I Division assessed over $715 million,

averaging approximately $329,257 per return and approximately $2,157 per hour.

24

Figure 4

shows the percentage of closed examinations in the LB&I Division, for individual taxpayers with

TPI of $10 million or more selected by the HII model, the GHW model and all other methods for

TYs 2016 through 2021, as of June 30, 2023.

Figure 4: LB&I Division Closed Examinations of Individual Tax Returns with TPI of $10 Million or

More by Selection Method for TYs 2016 Through 2021

25

Source: TIGTA’s analysis of closed tax return examinations as of June 30, 2023, per A-CIS Data provided

by the IRS.

As previously stated, the IRS began addressing the 2020 Treasury Directive starting with the

TY 2018 audit rate goal, primarily due to statute of limitation issues. Therefore, we consider

examinations of individual tax returns with TPI of $10 million or more for TYs 2016 and 2017 as

pre-Treasury Directive. As shown in Figure 4, prior to the 2020 Treasury Directive,

i.e.

, TYs 2016

and 2017, LB&I Division’s selection of individual tax returns with TPI of $10 million or more for

examination primarily came from selection methods outside of the GHW program. A definite

shift in LB&I’s selection of these high-income returns is apparent beginning with TY 2018 (the

first tax year impacted by the 2020 Treasury Directive) where the HII model was responsible for

most of the returns selected.

Across these selection methods, we found that LB&I examination results were better in TYs 2016

and 2017, before modifications were made to the selection methodology based on the issuance

23

For TYs 2016 through 2021, the “other” category includes selection methods for various work streams such as Joint

Committee, captive insurance, and S Corporation distribution.

24

The amount assessed is the sum of the total positive dollars recommended. Therefore, all audits that result in a

refund would be reported as zero.

25

LB&I is currently in the process of auditing returns for TYs 2019 through 2021, so values for these TYs are subject to

change.

Page 11

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

of the 2020 Treasury Directive, than in

subsequent tax years.

26

Figure 5 compares

the no change rate by case selection

method for individual returns with TPI of

$10 million or more for TYs 2016 and 2017

(pre-directive) to TYs 2018 through 2020

(post-directive).

27

The no change rate for the GHW selection

model and the HII selection model (used in

TYs 2018 through 2020) has increased since

TY 2016. The no change rate for audits

selected through “other” methods has

decreased. It is possible that the no change

rate for TYs 2019 through 2020 may decrease,

as audits are still in process for these tax years.

IRS management stated that no change

examinations typically take less time to

complete than examinations requiring

adjustments. As the examination cycle

progresses for a particular tax year, the no

change rate will typically decrease as audits

requiring adjustments are completed.

26

As of June 30, 2023, the LB&I Division had closed only four examinations of individual taxpayers with TPI of

$10 million or more for TY 2021, therefore, due to limited data, we excluded this tax year from our analysis as shown

in Figures 5 through 7.

27

After June 30, 2023, the LB&I Division continues to audit returns for TYs 2019 through 2020, therefore the values

for those tax years, as shown in Figures 5 through 7, are subject to change.

Source: TIGTA’s analysis of closed tax return

examinations as of June 30, 2023, per A-CIS data

provided by the IRS.

Figure 5: Examinations of Returns with TPI $10

Million or More Were Less Productive After

Selection Method Modifications Were Made in

Response to the 2020 Treasury Directive

Page 12

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Figure 6 compares the average dollars assessed per return by case selection method for

individual returns with TPI of $10 million or more for TYs 2016 and 2017 (pre-directive) to

TYs 2018 to 2020

(post-directive).

As Figure 6 shows, the average dollars

assessed per return with TPI of $10 million

or more was nearly six times more

productive prior to the 2020 Treasury

Directive.

Figure 7 compares the average dollars

assessed per hour by case selection

method for individual returns with TPI of

$10 million or more for TYs 2016 and 2017

(pre-directive) to TYs 2018 to 2020

(post-directive) in the LB&I Division.

As shown in Figure 7, the average dollars

assessed per hour on returns with TPI of

$10 million or more were nearly 14 times

more productive prior to the 2020 Treasury

Directive. Overall, we found that the no

change rate was lower and average dollars

assessed per return and the average dollars

assessed per hour were higher in TYs 2016 and

2017 prior to the 2020 Treasury Directive.

LB&I Division management stated that factors

such as attrition and workforce played a role in

the no change rate, citing significant attrition

of 5 to 10 percent per year with less agents

available to open new cases to meet goals.

Management added that cases changed hands

many times as agents left, adding to high cycle times and a higher likelihood of cases closing

due to statute of limitation issues. The Division’s FY 2022 and third quarter FY 2023 Key Stat

reports noted that the number of staff years applied to all LB&I returns went from approximately

1,616 staff years in FY 2018 to approximately 937 as of June 2023, suggesting that their

workforce has decreased during that time. Additionally, according to a TIGTA report released in

August 2023, at the end of FY 2019 there were 3,040 revenue agents in LB&I and as of

Figure 6: The Average Dollars Assessed per

Return with TPI of $10 million or more were

Nearly 6 Times More Productive Prior to the

2020 Treasury Directive

Source: TIGTA’s analysis of closed tax return

examinations as of June 30, 2023, per A-CIS data

provided by the IRS.

Source: TIGTA’s analysis of closed tax

return examinations as of June 30, 2023,

per A-CIS data provided by the IRS.

Figure 7: The Average Dollars Assessed

per Hour with TPI of $10 million or more

were Nearly 14 Times More Productive

Prior to the 2020 Treasury Directive

Page 13

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

March 31, 2023, there were 2,908 in LB&I, which is a 4.3 percent decrease.

28

Management also

shared that the new Bipartisan Budget Act of 2015 centralized partnership audit regime

procedures were not always clear and resulted in premature closures for a variety of issues

thereby contributing to the increased no change rate.

29

The IRS’s primary objective in selecting returns for examination is to promote the highest degree

of voluntary compliance on the part of taxpayers. This requires the exercise of professional

judgement in selecting sufficient returns of all classes to assure taxpayers receive equitable

consideration by using available experience and statistics indicating the probability of

substantial error, and in making the most efficient use of examination staffing and other

resources.

30

As detailed above, there are multiple factors influencing the LB&I Division’s increasing no

change rates and lower productivity measures.

31

Ultimately, all factors should be considered in

reviewing the methods used by the LB&I Division to select returns for examination to promote

the highest degree of voluntary compliance and efficient use of limited resources. Also, if the

IRS continues to select returns of taxpayers who are compliant, this imposes an unfair burden on

those taxpayers.

Recommendation 2: The Commissioner, Large Business and International Division, should

identify the potential causes for the low productivity examination results and monitor the

productivity measures related to the highest income individual taxpayers including those with

TPI of $10 million or more, ensuring the most productive returns are selected for examination.

Management’s Response: The IRS partially agreed with this recommendation with

respect to the need to identify potential causes for the low productivity examination

results and stated that it had already taken steps to identify the causes. The IRS plans to

use enhanced data and analytics to select cases based on the highest risk of

noncompliance.

Office of Audit Comment: Although the IRS partially agreed with this

recommendation, it did agree to monitor productivity measures related to

high-income high-wealth taxpayers, including those with TPI of $10 million or

more, to ensure the most productive returns are selected for examination. In

combination with the IRS’s response to Recommendation 1 and this

recommendation that includes identifying the potential causes for the low

productivity examination results, the collective actions taken should fully address

this recommendation.

28

TIGTA, Report No. 2023-30-054,

The IRS Needs to Leverage the Most Effective Training for Revenue Agents

Examining High-Income Taxpayers

p. 10 (Aug. 2023).

29

Pub. L. No. 114-74, § 1101, 129 Stat. 625.

30

Internal Revenue Manual 1.2.1.5.10(2) (June 1, 1974).

31

LB&I management stated that other factors including workload may also impact the increasing no change rates

and lower productivity measures. We did not review workload levels in this audit.

Page 14

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

The IRS Overstated the Opportunity Costs Associated With the 2020 Treasury

Directive

On March 13, 2020, the then IRS Commissioner responded to the then Secretary of the Treasury

citing the resource needs of at least 400 full-time revenue agents, with the majority being at

General Schedule Grade 13 level. The then Commissioner also cited the following opportunity

costs associated with complying with the 2020 Treasury Directive:

• Approximately 900 fewer audits of large and mid-size business returns.

• 600 fewer audits of small corporate returns.

• 850 fewer audits of individual returns with TPI under $10 million.

The then Commissioner was stating that a total of 1,500 business returns and 850 individual

returns could not be worked if the 2020 Treasury Directive were undertaken, since resources

would need to be reallocated to work the additional returns required to meet the Directive. Our

review identified that these stated opportunity costs were based on the additional examinations

(not including in process or planned examinations) required to collectively meet the 2020

Treasury Directive for TYs 2017 and 2018.

We reviewed the IRS’s calculations to determine the opportunity costs for working on individual

returns with TPI of $10 million or more. At the time of the IRS’s response, the IRS had already

started or planned to start about 45 percent of the audits it would need to complete to reach

the 8 percent audit rate for TYs 2017 and 2018 combined.

The IRS provided us with the methodology used by the SB/SE Division to determine how it

identified approximately 600 fewer small corporate returns and about 850 fewer audits of

individual returns with TPI under $10 million would be conducted in TYs 2017 and 2018, for the

IRS to complete the additional audits necessary to reach the 8 percent audit rate goal of audits

over $10 million TPI. However, the IRS did not provide us with the methodology used by the

LB&I Division to determine how it identified that about 900 fewer large and mid-size business

audits would be conducted. The IRS stated that it did not have the exact computations that led

to the figure. As a result, for our assessment, we used information from the FY 2019 LB&I Key

Stats report to calculate how many large and mid-size business audits the IRS would need to

forego to complete the additional audits necessary to achieve the 8 percent audit rate for

TYs 2017 and 2018. We determined that the IRS would work approximately 710 fewer

combined large and mid-size business audits, which is 190 less audits than the 900 audits

documented in the then Commissioner’s March response. Therefore, the opportunity costs

appear to be overstated.

When we asked what the retention policy is for the calculations used in the Commissioner’s

memorandum, we were provided with the IRS General Records Schedule, which states that

common office records or administrative records maintained by any agency office can be

destroyed once there ceases to be a business use. However, according to Federal Records

Management, records that are evidence of an agency’s decisions must be managed properly for

the agency to function effectively and to comply with Federal laws and regulations and as such,

“the head of each Federal agency shall make and preserve records containing adequate and

proper documentation of the organization, functions, policies, decisions, procedures, and

essential transactions of the agency and designed to furnish the information necessary to

Page 15

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

protect the legal and financial rights of the Government and of persons directly affected by the

agency’s activities.”

32

If the support for information reported in the Commissioner’s

memorandum is not maintained, then there is no way to determine if the data in the

memorandum is accurate because there is no way to verify the accuracy of the calculations used

to determine these figures.

32

Records Management by Federal Agencies, Pub. L. 90–620, 82 Stat. 1297 (codified as amended in 44 United States

Code Section 3101).

Page 16

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Appendix I

Detailed Objective, Scope, and Methodology

The overall objective of this audit was to determine whether the IRS was meeting the

Department of the Treasury’s established goal of auditing a minimum of 8 percent of all

high-income individual returns filed each year.

1

To accomplish our objective, we:

• Assessed the IRS’s processes and procedures for selecting high-income returns for audit,

including reviewing the Internal Revenue Manual, programming guides, and interviewing

IRS Management to determine how the IRS selected high-income tax returns for audit,

along with understanding any differences between the SB/SE and LB&I Divisions’

processes.

• Determined if any changes were made to the process once the Treasury Directive was

issued in February of 2020.

• Reviewed the IRS’s calculations of audit rates for high-income tax returns for TYs 2016

through 2021.

• Reviewed the results of the audits performed to determine the productivity and manner

of disposition for each audit. We also compared the productivity of high-income audits

to audits of returns with TPI less than $10 million for both the SB/SE and the LB&I

Divisions. Additionally, we compared the productivity measures of high-income audits

conducted by the LB&I Division based on selection methods.

• Reviewed the IRS Strategic Operation Plan and interviewed management on their plans

to monitor and evaluate examination results of the highest income individual taxpayers,

including those with TPI of $10 million or more.

• Validated available IRS information supporting the then Commissioner’s March 2020

response to the Secretary of the Treasury reflecting the opportunity costs of shifting

resources to meet the 2020 Treasury Directive.

Performance of This Review

This review was performed with information obtained from the Headquarters offices of the

SB/SE Division located in Lanham, Maryland and the LB&I Division located in Washington, D.C.,

during the period February 2023 through March 2024. We conducted this performance audit in

accordance with generally accepted government auditing standards. Those standards require

that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a

reasonable basis for our findings and conclusions based on our audit objective. We believe that

the evidence obtained provides a reasonable basis for our findings and conclusions based on

our audit objective.

Major contributors to the report were Phyllis Heald London, Acting Assistant Inspector General

for Audit (Compliance and Enforcement Operations); Michele Jahn, Director; Javier Fernandez,

1

Our audit focused on IRS examinations of individual returns with total positive income of $10 million or more, which

the IRS used to comply with the minimum 8 percent audit rate goal.

Page 17

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Audit Manager; Aranxa Delgado, Lead Auditor; Stephanie Finlay, Lead Auditor; Yancy Tam,

Auditor; and Laura Christoffersen, Information Technology Specialist.

Data Validation Methodology

We performed tests to assess the reliability of data from the A-CIS. We evaluated the data by

(1) performing electronic testing of required data elements, (2) reviewing existing information

about the data and the system that produced them, (3) interviewing agency officials

knowledgeable about the data, (4) reconciling selected data to the Integrated Data Retrieval

System. We determined that the data were sufficiently reliable for purposes of this report.

Internal Controls Methodology

Internal controls relate to management’s plans, methods, and procedures used to meet their

mission, goals, and objectives. Internal controls include the processes and procedures for

planning, organizing, directing, and controlling program operations. They include the systems

for measuring, reporting, and monitoring program performance. We determined that the

following internal controls were relevant to our audit objective: the IRS’s policies, procedures

and practices related to the selection of individual returns for examination by the SB/SE and

LB&I Divisions. We evaluated these controls by interviewing management, reviewing reports,

and analyzing closed examination data.

Page 20

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 21

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 22

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 24

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 26

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 27

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 28

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Page 29

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Appendix VI

Glossary of Terms

Term Definition

Activity Code A code that identifies the type and condition of returns selected for audit.

Audit Information

Management System –

Centralized Information

System

A database that provides monthly Audit Information Management System

data on both open and closed cases.

Discriminant Index

Function

A mathematical technique used to computer-score income tax returns as to

examination potential. Examination potential is indicated by a numeric

score that is assigned to each return by examination class; the greater the

score, the greater the examination potential within each examination class.

Fiscal Year

Any yearly accounting period, regardless of its relationship to a calendar

year. The Federal Government’s fiscal year begins on October 1 and ends

on September 30.

General Schedule

The classification and pay system established under 5 United States Code

Chapter 51 and Subchapter III of Chapter 53. It is a rate of basic pay for

professional, technical, administrative, and clerical professionals working for

the Federal Government.

Revenue Agent

Employees in the Examination function who conduct face-to-face

examinations of more complex tax returns, such as businesses,

partnerships, corporations, and specialty taxes.

Tax Year

A 12-month accounting period for keeping records on income and

expenses used as the basis for calculating the annual taxes due. For most

individual taxpayers, the tax year is synonymous with the calendar year.

Total Positive Income

The sum of all positive amounts shown for the various sources of income

reported on the individual tax return and, therefore, excludes losses.

Page 30

The IRS Ceased Compliance With the $10 Million Taxpayer Treasury

Directive in Favor of an Overall Focus on High-Income Taxpayer Noncompliance

Appendix VII

Abbreviations

A-CIS Audit Information Management System – Centralized Information System

CIP Compliance Initiative Project

FY Fiscal Year

GHW Global High Wealth

HII High-Income Individual

IRS Internal Revenue Service

LB&I Large Business and International

SB/SE Small Business/Self-Employed

TIGTA Treasury Inspector General for Tax Administration

TPI Total Positive Income

TY Tax Year

To report fraud, waste, or abuse,

contact our hotline on the web at www.tigta.gov

or via e-mail at

oi.govreports@tigta.treas.gov.

To make suggestions to improve IRS policies, processes, or systems

affecting taxpayers, contact us at www.tigta.gov/form/suggestions

.

Information you provide is confidential, and you may remain anonymous.